On March 14 (local time), global credit rating agency Moody's downgraded SK Innovation's credit rating from 'Baa3' to 'Ba1'. Baa3 was the lowest investment-grade rating, and this adjustment signifies a downgrade to below investment grade. Moody's cited "continued underperformance in the battery sector (SK On) and high debt burden" as reasons.

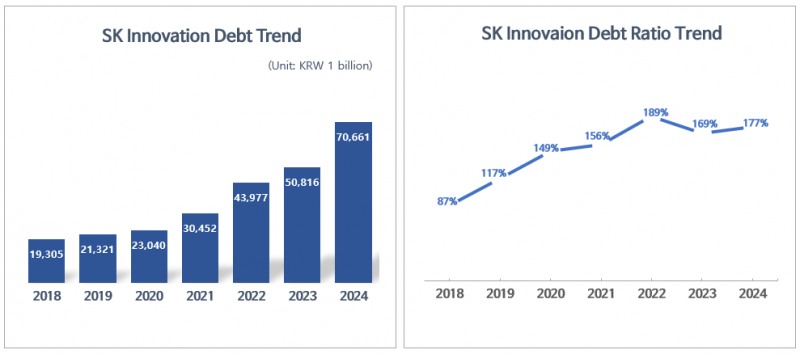

SK Innovation's financial burden has increased dramatically since 2020, largely due to increased borrowing for battery investments. The company's debt ratio has been on an upward trend: 87% in 2018, 149% in 2020, 189% in 2022, and 177% in 2024. Although it decreased slightly last year due to the merger with SK E&S, it remains at a level requiring management compared to other energy and battery companies maintaining ratios around 100%.

The poor profitability of the battery business could also negatively impact domestic credit ratings. Korea Ratings currently maintains SK Innovation's credit rating at AA (stable). One of the factors for a credit rating downgrade is "if the ratio of net borrowings to EBITDA (earnings before interest, taxes, depreciation, and amortization) consistently exceeds 7 times".

According to SK Innovation's IR materials, as of the end of last year, the company's net borrowings were KRW 27.5266 trillion, with an EBITDA of KRW 276.4 billion. The net borrowings to EBITDA ratio stands at 10.3 times, meeting the criteria for a credit rating downgrade.

관련기사

'Solid Performance Amidst Recession' - S-Oil · GS Caltex, What’s Their Secret?LG Energy Solution, Samsung SDI, SK On Brace for Prolonged EV Battery SlumpSK Innovation KRW -160 billion, S-Oil KRW -430 billion... Earnings shock predicted for refinery businessSK Innovation-SK E&S Merger Over Final ThresholdLast Year’s Jackpot, Pharma Firms Bet Everything on the Next Blockbuster Drug

데일리 금융경제뉴스 Copyright ⓒ 한국금융신문 & FNTIMES.com

저작권법에 의거 상업적 목적의 무단 전재, 복사, 배포 금지

가장 핫한 경제 소식! 한국금융신문의 ‘추천뉴스’를 받아보세요~

{kind=link}

{kind=link}