이미지 확대보기

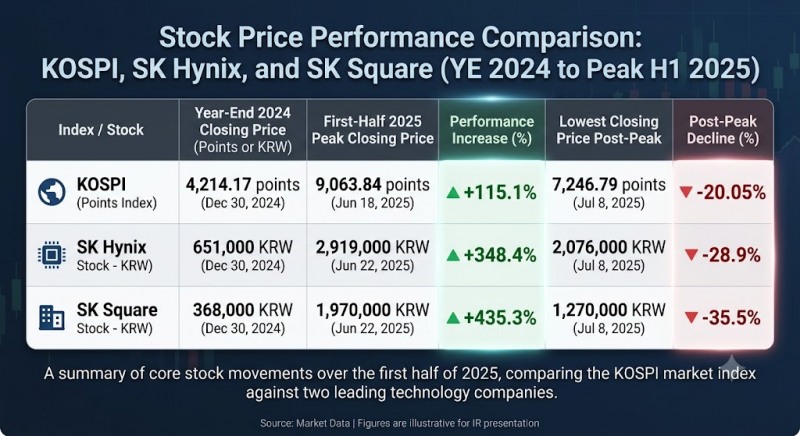

이미지 확대보기While the KOSPI index rose 72% from the end of 2025, SK Square's share price surged 261%, from KRW 368,000 to KRW 1,327,000 based on the closing price on the 9th. Compared with its low point at the end of June last year, the increase reaches as much as 625%. On the other hand, the share price, which had soared to an intraday high of KRW 2,189,000 on June 23, has plunged nearly 40% from that peak.

There is a common denominator behind this repeated pattern of rises and falls: investors are effectively valuing SK Square as "a company whose value is tied to its stake in SK Hynix." Indeed, most of its core indicators — corporate value, earnings, dividends, and even credit rating — are concentrated in SK Hynix.

이미지 확대보기

이미지 확대보기Launched as an Investment Specialist Firm, But Its Share Price Ultimately Follows Hynix

SK Square (CEO Kim Jung-kyu) was launched in November 2021 through a spin-off of SK Telecom. The telecommunications business remained with the surviving entity, SK Telecom, while the semiconductor and ICT investment division was separated to form an investment specialist company. It originally aimed to be an investment holding company that would expand new investments centered on semiconductors, platforms, and digital infrastructure.However, the market currently sees things differently. Securities firms assess that the vast majority of SK Square's corporate value stems from its stake in SK Hynix. Yuanta Securities recently estimated SK Square's net asset value (NAV) at approximately KRW 347 trillion, of which the value of its SK Hynix stake was estimated to account for KRW 342 trillion.

For this reason, issues surrounding SK Hynix are immediately reflected in SK Square's share price. A representative case is SK Hynix's American depositary receipt (ADR) listing on the Nasdaq. When Hynix resolved to pursue the listing on June 24, expectations grew for expanded access by overseas investors. Analysis emerged suggesting that Hynix's valuation, which had been undervalued domestically, would be reassessed against global semiconductor companies, and buying interest flowed into SK Square as well.

관련기사

SK's Holding Subsidiaries Diverge: SK Discovery Falls Behind the PackBeyond Hynix: SK's Three-Company AI Alliance Eyes Full-Stack Jackpot'Stock Price Soars' SK Square… Expectations Rise for 'AI & Semiconductor' Investments [KFT Topic]SK Hynix Weighs Growth Over Governance in Treasury Share Strategy [Treasury Share Report]SK hynix Eyes KRW 40 Trillion in Q1 Operating Profit — Is AI Ushering in a Long-Term Boom?

Yuanta Securities analyst Lee Seung-woong maintained a target price of KRW 2.1 million in a report on the 7th, saying that if SK Hynix's ADR listing narrows the valuation gap with global peers, it could lead to a rise in SK Square's NAV. He also positively noted that the NAV discount rate had narrowed from around 70% to the 40% range, driven by sustained share buybacks and cancellations since the listing announcement.

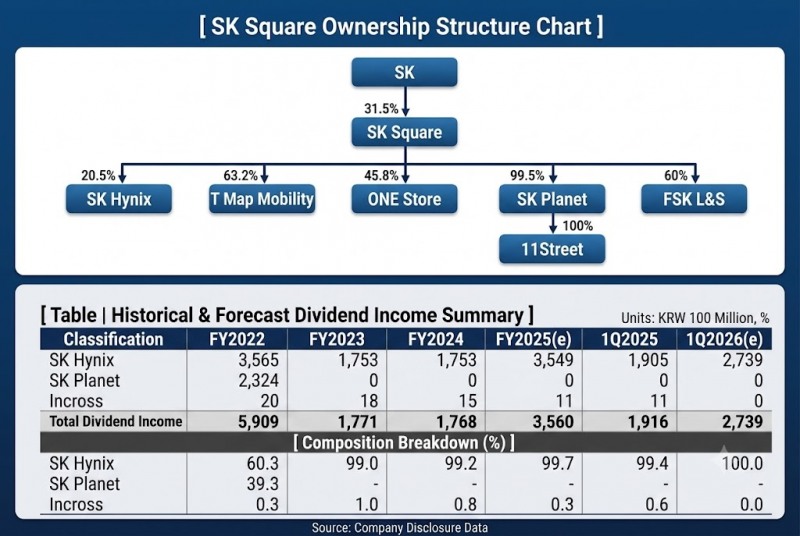

That said, not all factors are positive. On the 6th, SK Hynix disclosed an adjustment to the planned issue price for its new ADR shares, lowering it from an initial KRW 2,555,000 to KRW 2,425,000. While this reflects the recent share price correction, the market interpreted it as a signal of lowered valuation expectations. The new share issuance will also dilute existing shareholders' stakes. SK Square's stake in Hynix, which stood at 20.5% as of June 23, is expected to fall to around 20%.

In addition, concerns over slowing memory demand — which emerged following Apple's product price increases — weighed on semiconductor stocks broadly, dragging down SK Square's share price as well.

Portfolio restructuring is also underway. On the 29th of last month, SK Square sold its entire 45.78% stake in ONE Store, removing it from its subsidiaries. Although the asset was not large in proportion, the move is seen as simplifying the portfolio and partially resolving risks related to financial investors (FIs).

Earnings and Dividends, Too, Point to Hynix... The Numbers Tell the Story of "Concentration"

On a consolidated basis, SK Square recorded revenue of KRW 1.4115 trillion, operating profit of KRW 8.7974 trillion, and net income of KRW 8.8187 trillion last year. In the first quarter of this year as well, it posted revenue of KRW 300.3 billion, operating profit of KRW 8.2783 trillion, and net income of KRW 8.3747 trillion. However, these results reflect the performance of SK Hynix, which is consolidated into SK Square's accounts, rather than SK Square's own business.Looking at SK Square's separate (non-consolidated) financial statements, the concentration in its revenue structure is stark. According to NICE Investors Service, SK Hynix's share of SK Square's dividend income rose from 60.3% in 2022 to 99.0% in 2023, 99.2% in 2024, and 99.7% in 2025. In the first quarter of this year, the entirety of dividend income came from SK Hynix.

이미지 확대보기

이미지 확대보기By contrast, major unlisted subsidiaries are struggling with poor profitability. As of 2025, operating margins stood at -5.0% for T map Mobility, -4.6% for Content Wavve, and -1.6% for SK Planet. Content Wavve is in a state of complete capital impairment, with total equity of negative KRW 146.7 billion.

Credit rating agencies point to this business structure as a core risk. NICE Investors Service and Korea Ratings assessed that SK Square's financial stability depends absolutely on SK Hynix's competitiveness and dividend capacity. Indeed, the basis for calculating the company's own credit rating is also Hynix's credit rating.

A distinctive feature is also evident in cash flow. SK Square posted net income in the KRW 8 trillion range in the first quarter of this year, but its consolidated free cash flow (FCF) came to negative KRW 245.3 billion. This is not the result of a decline in SK Square's own cash-generating ability, but rather reflects, in the consolidated financial statements, the cash outflow arising from SK Hynix's large-scale capital expenditure (CAPEX) on its Yongin cluster and packaging plant.

Three Challenges Ahead: ADR, Shareholder Returns, and Portfolio

Securities firms expect that, for the time being, SK Square's share price will continue to respond most sensitively to changes in SK Hynix's corporate value.The market expects that if Hynix's ADR listing narrows the valuation gap with global semiconductor companies, SK Square's corporate value will also be reassessed. At the company level, SK Square has announced shareholder return plans for this year, including share buybacks worth KRW 110 billion and cash dividends worth KRW 200 billion. Earlier, in May, it completed a KRW 40 billion share buyback.

That said, over the medium to long term, the performance of major subsidiaries other than Hynix is also expected to affect corporate value. While the sale of ONE Store has partially simplified the portfolio, improving the profitability of major unlisted subsidiaries such as T map Mobility, Content Wavve, and SK Planet remains a challenge.

Ultimately, SK Square's corporate value hinges on three axes: SK Hynix's valuation, the pace of shareholder return policy execution, and improvement in unlisted subsidiaries' earnings. For now, market assessment following the ADR listing will drive the share price, but over the medium to long term, proving the competitiveness of its investment portfolio beyond Hynix will be the test of its corporate value.

Doo KyoungWoo (kwd1227@fntimes.com)

데일리 금융경제뉴스 Copyright ⓒ 한국금융신문 & FNTIMES.com

저작권법에 의거 상업적 목적의 무단 전재, 복사, 배포 금지

가장 핫한 경제 소식! 한국금융신문의 ‘추천뉴스’를 받아보세요~

{kind=link}

{kind=link}

{kind=link}