이미지 확대보기

이미지 확대보기Hyundai Mobis is the core parts affiliate of the Hyundai Motor Group. It supplies modules and components to Hyundai Motor and Kia, showing a stable revenue flow. Looking at the trend of the Altman Z-Score — a model for predicting corporate financial risk — the company has maintained a "safe zone."

However, viewed differently, this also points to clear structural limitations tied to the group's dependency and the finished-vehicle sales cycle. While there are significant advantages to being a finished-vehicle parts affiliate, the reality is that the company has failed for years to achieve a value-up breakthrough above its ceiling.

A Steady, Unremarkable Performer

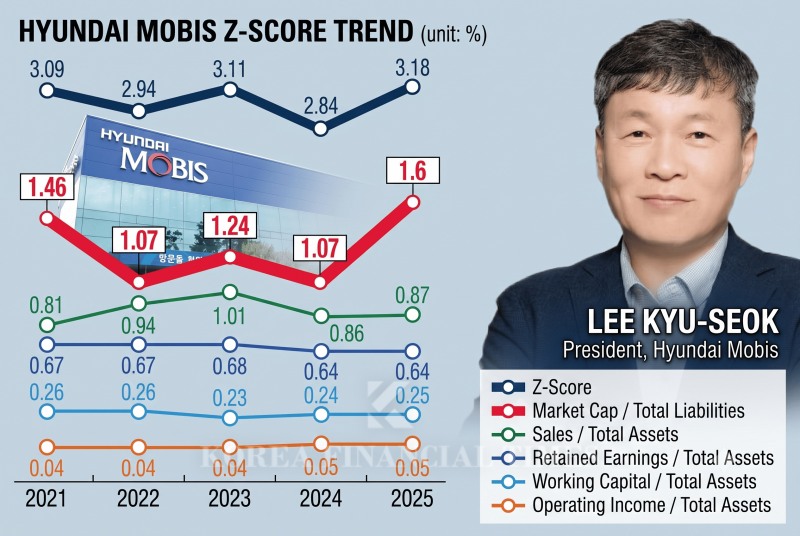

According to THE COMPASS, an AI-based data analysis platform built in-house by Korea Financial Times, Hyundai Mobis' Z-Score came in at ▲3.09 in 2021, ▲2.94 in 2022, ▲3.11 in 2023, ▲2.84 in 2024, and ▲3.18 in 2025. The score has fluctuated within a range of 2.84 to 3.18, generally showing a pattern of returning to the safe zone.The Z-Score is a model that predicts the likelihood of corporate bankruptcy, calculated based on financial statement items (X1 [working capital/total assets] + X2 [retained earnings/total assets] + X3 [operating income/total assets] + X4 [market capitalization/total liabilities] + X5 [sales/total assets]). For manufacturers, a score of 3 or above is considered a safe zone, while a score below 1.8 is considered a risk zone.

관련기사

Robot Joints, 80%-a-Year Growth: Hyundai Mobis, Samsung Electro-Mechanics Lead Korea's Actuator Rush [K-Humanoid Wars ④]Hyundai Mobis Posts Record Results, Pivots to Robotics and Electrification [KFT Topic]Hyundai Motor Group Chairman Mulls Deepening Boston Dynamics IPO DilemmaHyundai Motor Faces Massive Union Bonus Demand Exceeding Dividends Amid Heavy Tech InvestmentsShareholder Returns or Succession Strategy? The Dual Purpose Behind Hyundai Motor and Kia's Payout Policies

Among the components of the company's Z-Score, the contribution of "market capitalization to total liabilities ratio (X4)" stands out most prominently at 30.2%. This is because, with Hyundai Motor and Kia as a solid "backing" generating stable cash flow and profits, other financial indicators such as retained earnings, operating income, and sales also show gentle trends.

Hyundai Mobis' operating profit actually expanded from roughly KRW 2 trillion in 2021 to KRW 3.3574 trillion last year. Over the same period, retained earnings grew by approximately KRW 11 trillion, from about KRW 34 trillion to KRW 45 trillion. Meanwhile, the debt ratio has been managed at a level of 43-44% each year.

Market capitalization, separate from earnings, fluctuates significantly depending on the business environment or expectations for the company's growth. In 2022 and 2024, when Hyundai Mobis' Z-Score fell into the 2-point range, both years showed a pattern similar to a decline in the X4 figure. Hyundai Mobis' X4 figure fell from 1.49 in 2021 to 1.07 in 2022, rebounded to 1.24 in 2023, and then fell again to 1.07 in 2024.

Transition to a Robotics Parts Supplier

Ultimately, it can be said that Hyundai Mobis' Z-Score is likely to break through its ceiling going forward depending on the company's stock price — that is, on the outcome of its value-up efforts.Since unveiling the humanoid robot "Atlas," developed by its robotics affiliate Boston Dynamics, in January of this year, Hyundai Motor Group has been pursuing a major transformation into a robotics company. Starting in 2028, the group plans to deploy Atlas at its North American production base and expand its use into factory automation and other industries.

In line with this trend, Hyundai Mobis is attempting to transition from a finished-vehicle parts supplier to a robotics parts supplier. Building on its vehicle parts design capabilities and accumulated mass-production experience, the company has decided to first enter the robot actuator market.

An actuator is a core drive device that performs movement based on signals received from a controller, and it is a key component accounting for roughly 60% of the material cost of manufacturing a humanoid robot.

Earlier this year, at CES 2026 in Las Vegas, Hyundai Mobis announced that it would produce and supply actuators for Atlas, revealing that it had secured a reliable customer.

As Hyundai Mobis shifts its positioning from an automotive parts supplier to a core axis of the robotics, semiconductor, and SDV (software-defined vehicle) parts ecosystem, there is ample room for its X4 ratio to rise as the market re-evaluates the company.

A Rosy Outlook Is Not Guaranteed

The question is whether this rosy future can actually materialize. Ideals and reality differ. The key issue is whether Hyundai Mobis can deliver results that meet market expectations.First, there is the matter of production capacity. Hyundai Motor has stated that it will produce Atlas at a rate of about 30,000 units annually by 2028. While Hyundai Mobis does plan to supply actuators for Atlas, it has never disclosed the exact scale of production involved.

It is also unclear whether profitability can be sustained, as component unit prices could fall as the robotics market expands. According to Hanwha Investment & Securities, the average unit price of an actuator is projected to fall from USD 2,000 in 2027 to USD 1,000 in 2028, and to USD 599 by 2032 — a decline to roughly 30% of the original price within five years.

The possibility of oversupply from China, which has declared its ambitions to dominate robotics, is another factor to watch. There is no shortage of precedents in which China-driven oversupply — in solar power, electric vehicles, batteries, and other sectors — eroded profitability.

The most recent such case is the battery industry. South Korean battery manufacturers such as LG Energy Solution and Samsung SDI grew by securing global market share on the strength of their technology, but were later squeezed on both market share and profitability by Chinese manufacturers' mass production and low pricing offensive.

Indeed, China's robotics industry is growing rapidly. According to the Korea Institute of Intellectual Property, of the 66 robot models unveiled between 2022 and 2024, 40 — or 61% of the total — were made by Chinese companies.

Kim Seong-rae, an analyst at Hanwha Investment & Securities, assessed that as robots enter the commercialization stage, the ability to deliver products that meet quality, cost, and delivery (QCD) standards will emerge as a key competitive factor.

The outcome of vague expectations about future value can be seen in Hyundai Mobis' stock price. As expectations for the robotics transition have narrowed and challenges emerging after commercialization have come into focus, the stock has recently turned downward.

Hyundai Mobis shares, which started this year at KRW 373,000, rose as high as KRW 822,000 on June 1 following CES. However, the closing price on July 3 was KRW 494,000 — a drop of 39.9% in a single month.

An industry official at an investment bank said that new challenges have recently emerged, including performance tied to Boston Dynamics' Atlas and future cost competition in robotics, adding that the recent stock price trend also reflects investors losing confidence as they weigh the situation after commercialization.

Kim JaeHun (rlqm93@fntimes.com)

데일리 금융경제뉴스 Copyright ⓒ 한국금융신문 & FNTIMES.com

저작권법에 의거 상업적 목적의 무단 전재, 복사, 배포 금지

가장 핫한 경제 소식! 한국금융신문의 ‘추천뉴스’를 받아보세요~

{kind=link}