이미지 확대보기

이미지 확대보기The government and the country's naphtha cracking center (NCC) operators have been pushing for restructuring of the domestic petrochemical industry since the second half of last year. Among Korea's three major petrochemical complexes — Daesan, Yeosu, and Ulsan — Ulsan has seen the slowest progress. This is because the three companies based there — SK Geo Centric, Korea Petrochemical, and S-Oil — have divergent interests.

SK Geo Centric is in the camp that agrees on the need to reduce NCC capacity. Its facilities are relatively aged, and the company holds that a mid-to-long-term structural overhaul is needed in tandem with a rebalancing of its group portfolio. S-Oil, by contrast, is reluctant to cut NCC capacity. This is because it judges that the new facilities of its "Shaheen Project," which will begin full-scale operation early next year, have sufficient price competitiveness even compared with Chinese players.

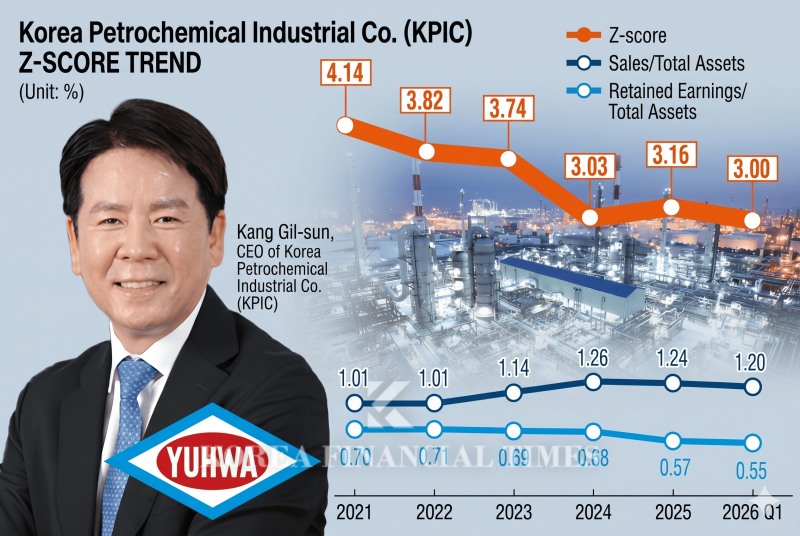

The company has among the strongest financial soundness of Korea's major NCC operators. According to "THE COMPASS," the artificial intelligence (AI) data platform developed in-house by the Korea Financial Times, Korea Petrochemical's Altman Z-Score stood at 3.0 as of the first quarter of this year. The Z-Score is a financial-soundness indicator that predicts the risk of corporate bankruptcy; a reading of 3.0 or higher is assessed as the "safe" zone, indicating a very healthy financial condition.

Compared with other domestic NCC operators such as Lotte Chemical (1.07) and LG Chem (0.98) — which have been struggling amid the oversupply originating from China since 2022 and have already entered the "distress" zone below 1.18 — it is immediately clear just how strong Korea Petrochemical's financial soundness is.

관련기사

[Petrochemicals: A Shifting Landscape] Korea's Petrochemical Restructuring Accelerates as Middle East Crisis BitesLotte-HD Hyundai Daesan Merger Signals Full-Scale Petrochemical Restructuring in KoreaLotte Chemical Swung to Profit in Q1 — So Why Won't the Stock Move?Lotte Chemical Snaps 10-Quarter Deficit Streak... How Long Will War-Driven Windfall Last?Kumho Petrochemical's Treasury Shares Face Governance Test After 20 Years [Treasury Share Report]

An item that illustrates this well is X5 (sales / total assets). This quarter, that value was 1.2, accounting for 40% of the total. This means Korea Petrochemical generated sales efficiently despite holding NCC facilities more than 30 years old.

That said, Korea Petrochemical too has seen its financial soundness gradually deteriorate, posting losses for three consecutive years from 2023 to 2025. Its annual Z-Score fell from 4.14 in 2021 to 3.0 in the first quarter of this year. In particular, the X2 (retained earnings / total assets) and X3 (operating profit / total assets) items, which reflect profitability, dropped sharply.

The adage may be "earn in the boom, endure the bust," but the company can no longer prepare for the future with such a strategy. That is because, with the oversupply from China shifting the petrochemical industry's paradigm, analysts say this downturn is not a temporary cycle but a structural slump. The later the timing of investment, the greater the risk of falling into a vicious cycle in which the capacity to invest in a transition to new businesses is depleted.

The risk of a key feedstock supplier turning into a competitor is also materializing. Korea Petrochemical sources naphtha, a petrochemical raw material, mainly from nearby S-Oil. If S-Oil expands its own petrochemical business through the operation of "Shaheen," the contractual relationship between the two companies could change. For Korea Petrochemical, it is a moment to consider reorganizing its supply chain.

It is not as though Korea Petrochemical has given no thought to restructuring its business. Hanju, an industrial gas and water supply company in which it had held an equity stake since the mid-2010s, was incorporated as a subsidiary last year through an additional increase in its stake. As a result, the company lowered the share of petrochemicals in its revenue from a previous level of 99% to around 80% currently. Given its high dependence on downstream industries, this is hard to view as a fundamental transformation of its business profile, but it amounts to a first step toward portfolio diversification.

One petrochemical industry official said, "Considering Korea Petrochemical's weight class, there are limits to an independent business transition," adding, "In the end, there will likely be no realistic card to play other than joining a restructuring in which government support can be expected."

Gwak Horyung (horr@fntimes.com)

데일리 금융경제뉴스 Copyright ⓒ 한국금융신문 & FNTIMES.com

저작권법에 의거 상업적 목적의 무단 전재, 복사, 배포 금지

가장 핫한 경제 소식! 한국금융신문의 ‘추천뉴스’를 받아보세요~

{kind=link}