이미지 확대보기

이미지 확대보기Parent Company Boards Given 'Five Key Obligations' and Subject to the '3% Rule'

According to industry sources on July 9, the Financial Services Commission (FSC) and the Korea Exchange (KRX) announced on July 6 revisions to exchange regulations and a new set of guidelines detailing the standards for "prohibiting duplicate listings in principle, with limited exceptions," opening a comment period that runs until July 14. The rules will take final effect after deliberation and approval by the Securities and Futures Commission (SFC) and the FSC's regular meeting.Under the guidelines, the board of a parent company pursuing the listing of a subsidiary must fulfill "five key obligations": ① assessing the impact on shareholders; ② devising shareholder protection measures; ③ confirming shareholder communication and consent; ④ holding a board vote for or against the listing and notifying the subsidiary; and ⑤ disclosure at each stage of the process. The KRX will then conduct a dedicated special review for duplicate listings.

Under the new guidelines, whether shareholder consent is required depends on how the subsidiary was established. General subsidiaries brought in through mergers and acquisitions (M&A) or newly founded can still pursue listing through the KRX's individual review process even without shareholder consent, and "low-weight subsidiaries" — those whose revenue, operating profit, and assets are all under 10% of the parent company's — are exempt from the shareholder consent requirement altogether.

However, regulators determined that subsidiaries created through physical division (spin-offs) require the strongest shareholder protections, given concerns over parent-company valuation discounts in the event of a duplicate listing. The FSC explained that even a low-weight subsidiary will be subject to mandatory shareholder consent if it was established through a physical division.

관련기사

Hyundai's IPO-Ready Boston Dynamics Runs Into Dual-Listing RoadblockLotte-HD Hyundai Daesan Merger Signals Full-Scale Petrochemical Restructuring in KoreaWhy LS Cable & System Won Korea's National Growth FundHanwha Solutions Trims Rights Offering Size, Shares Rebound — But KRW 600 Billion Shortfall RemainsWhy Hanwha Bought Back Into KAI After Seven Years

이미지 확대보기

이미지 확대보기HD Hyundai Robotics, LS Essex Solutions Among Those Affected

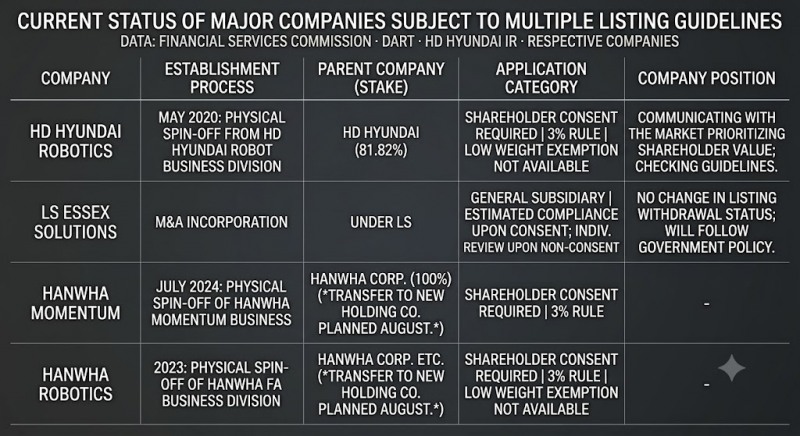

Among companies with planned IPOs, HD Hyundai Robotics is expected to be the most significantly affected. According to HD Hyundai's business report, HD Hyundai Robotics was established in May 2020 through the physical division of HD Hyundai's robotics business, and HD Hyundai currently holds an 81.82% stake in the company.Last year, HD Hyundai Robotics posted consolidated revenue of KRW 263 billion, accounting for just 0.4% of HD Hyundai's consolidated revenue of KRW 71.2594 trillion. The company recorded an operating loss of KRW 21.8 billion last year, followed by revenue of KRW 71.8 billion and an operating loss of KRW 5 billion in the first quarter of this year.

The company stated in its disclosures that the losses stem from expanded R&D investment aimed at strengthening its products and technology. In terms of scale, it is a textbook example of a low-weight subsidiary, but because it was established through a physical division, it does not qualify for the exemption. Should it pursue a listing in the future, it will be required to comply with the 3% rule.

Persuading general shareholders, however, is not expected to be easy. This is because LG Energy Solution — spun off from LG Chem — saw its parent company's share price remain depressed for an extended period after its 2022 listing.

In particular, the robotics business is viewed as having high growth potential, meaning a spin-off listing could affect the parent company's share price. HD Hyundai has projected that, amid growing expectations for expanded investment in physical AI, the global industrial robot market will grow roughly 7.7% this year to 619,000 units. The larger the market's expectations grow, the greater the pushback from parent-company shareholders is likely to be against spinning off a lucrative business for a separate listing.

In response, an HD Hyundai Robotics official said, "We will prioritize shareholder value and continue communicating with the market," adding, "Since the guidelines were only released yesterday, there is much to prepare for and confirm in line with the government's directives, so we are proceeding cautiously for now."

LS Group, whose subsidiary was brought in through M&A, faces comparatively less of a burden, but is likewise closely monitoring the situation. LS Essex Solutions — a wire-winding (copper wire wound around electronic devices) subsidiary under LS — withdrew its listing application this past January. None of the group's other subsidiaries reportedly have IPOs planned at this time.

An LS Group official said, "As the guidelines were only just released, nothing has changed regarding LS Essex Solutions' withdrawn listing," adding, "We will faithfully comply with government policy and continue to expand shareholder protection and communication; nothing has been decided regarding whether or when a listing might proceed."

Hanwha Momentum, Hanwha Robotics Would Be Affected If They Pursue Listings; Hanwha Energy 'Outside the Scope'

At Hanwha Group, Hanwha Momentum — a secondary battery equipment maker spun off from Hanwha Corporation's momentum division in July 2024 — and Hanwha Robotics — spun off from the FA business division in 2023 — would fall under the new rules if they pursue listings in the future.Both companies are set to become subsidiaries of the newly established "Hanwha Machinery & Service Holdings (tentative name)," to be created through a physical (human) division following approval at Hanwha Corporation's extraordinary shareholders' meeting on July 15 and formal establishment on August 1. In addition to Hanwha Momentum and Hanwha Robotics, the new holding company will also absorb the subsidiary-management functions of Hanwha Vision, Hanwha Hotels & Resorts, and Hanwha Galleria, with a relisting on the KOSPI market planned for August 25.

While the relisting via a human division — under which new shares are allocated to existing shareholders in proportion to their holdings — is not subject to the new duplicate-listing regulations, the shareholder consent requirement will apply if the two subsidiaries under the newly established holding company pursue their own listings in the future.

However, neither company reportedly has listing plans at this time. A Hanwha Group official said, "We have not heard of any listing possibility or plans for Hanwha Momentum, Hanwha Robotics, or the others."

Meanwhile, Hanwha Energy — an unlisted company controlled by the founding family — is not a subsidiary of a listed parent company and is therefore not subject to the new regulations.

Jung Jina (urzinnie@fntimes.com)

데일리 금융경제뉴스 Copyright ⓒ 한국금융신문 & FNTIMES.com

저작권법에 의거 상업적 목적의 무단 전재, 복사, 배포 금지

가장 핫한 경제 소식! 한국금융신문의 ‘추천뉴스’를 받아보세요~

{kind=link}

{kind=link}