이미지 확대보기

이미지 확대보기How the Combined KRW 250 Trillion Figure Was Calculated

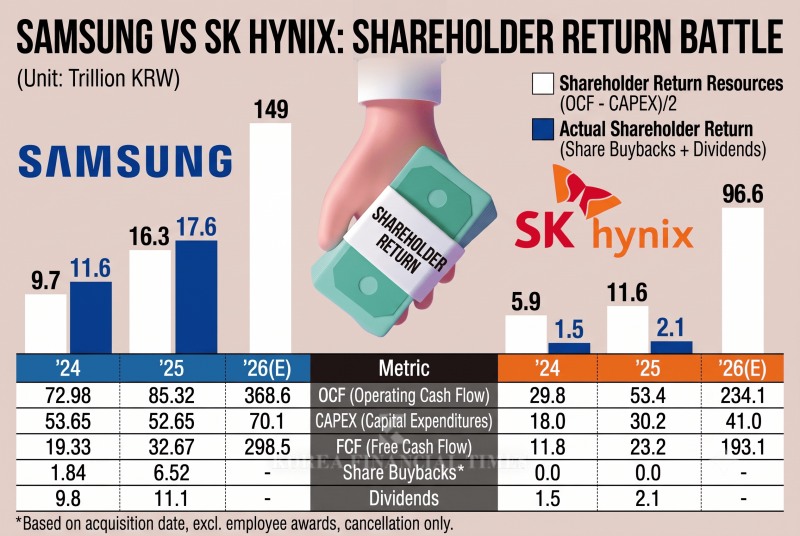

Samsung Electronics has signaled it will deliver the largest shareholder return in its history. The company adopted its current shareholder return policy in 2024, committing to return 50% of FCF to shareholders over a three-year period. This year — as the memory chip market enters a full-blown supercycle — marks the final year the policy will apply.FCF refers to the cash a company has left over after deducting essential expenditures from the money it earns. It is typically calculated by subtracting capital expenditures (CAPEX) — spending on tangible and intangible assets — from operating cash flow (OCF).

That year, Samsung Electronics spent KRW 11.1 trillion on dividend payments, including a special dividend of KRW 1.3 trillion. On share buybacks, excluding shares acquired for employee compensation purposes, KRW 6.52 trillion was spent specifically to enhance shareholder value through cancellation — including KRW 1.21 trillion in shares purchased in 2025 under the 2024 plan. Excluding that carryover amount, the remaining figure roughly matches the promised "50% of FCF" (KRW 16.3 trillion) earmarked for shareholder returns.

Recent brokerage estimates put Samsung Electronics' 2026 operating profit at around KRW 390 trillion — roughly nine times last year's operating profit of KRW 43.7 trillion. Based on that operating profit, OCF is estimated at around KRW 360 trillion to KRW 370 trillion.

관련기사

Why Samsung Lost Its Market-Cap Crown to SK hynixSamsung Electronics Surpasses 30% NAND Market Share, Bolsters 'Super-Gap' Lead Through NVIDIA AllianceSK hynix Eyes KRW 40 Trillion in Q1 Operating Profit — Is AI Ushering in a Long-Term Boom?Exynos Reborn: How Samsung Is Betting Its Chip Future on On-Device AI

Applying these projected OCF and CAPEX figures for this year, FCF is forecast at roughly KRW 300 trillion, putting the 50% shareholder return pool at around KRW 150 trillion. Were Samsung Electronics to return this entire amount purely through dividends, it would translate to roughly KRW 22,000 per share — about 13 times the KRW 1,668 per share paid in 2025. Based on the closing price of KRW 340,000 on June 24, that would imply a dividend yield of 6.5%, a level that is not unreasonable assuming subsequent share buybacks and cancellations are factored in as well.

SK hynix's shareholder return policy mirrors Samsung Electronics': 50% of FCF over three years. The difference is timing — SK hynix's policy began last year and runs through next year.

Last year, however, the policy was not fully carried out. Of the KRW 11.6 trillion earmarked for shareholder returns, only 18%, or KRW 2.1 trillion, was actually paid out as dividends. Under the original commitment, the remainder should be returned this year or next. This is widely interpreted as a result of SK hynix prioritizing the buildup of large cash reserves to fund its AI supercycle investments. In March, SK hynix CEO Kwak Noh-jung stressed that the company would secure KRW 100 trillion in net cash.

In 2026, however, SK hynix is expected to find it difficult to keep deferring shareholder returns. This year's operating profit alone is being projected at around KRW 280 trillion — roughly six times last year's level. Assuming CAPEX comes in at the mid-to-high KRW 40 trillion range, the resulting shareholder return pool would reach roughly KRW 100 trillion.

A Flood of Cash: Returns or Reinvestment?

Whether Samsung Electronics and SK hynix will actually return the combined KRW 250 trillion directly to shareholders is another matter entirely. After all, the commitments were made before anyone anticipated the current AI-driven boom.Semiconductors are also a cyclical industry, where companies typically reinvest boom-time earnings into CAPEX and R&D to widen their technological lead.

With both companies posting record share-price gains, some argue that shareholder returns need not be limited to dividends and share buybacks and cancellations.

If this year's CAPEX is increased two- to three-fold, the promised shareholder return amount would shrink accordingly. Samsung Electronics and SK hynix are reportedly in discussions with the government over building large-scale semiconductor plants in the Gwangju and South Jeolla Province area, with reports suggesting each company's investment could exceed KRW 200 trillion.

Other approaches are possible as well.

In a Samsung Electronics analyst report published on June 9, Mirae Asset Securities analyst Kim Young-gun laid out five possible shareholder return scenarios. Two of them involve a roughly KRW 100 trillion merger or acquisition (M&A). While acquisition costs are not directly booked as CAPEX, the acquired company's assets can be accounted for as CAPEX on the books. Such a scenario is not entirely implausible, given that Samsung Electronics set up a dedicated M&A team under its Business Support Task Force late last year and has been actively pursuing deals.

SK hynix's dilemma appears to run deeper. On June 16, The Korea Economic Daily reported that SK hynix was preparing a KRW 100 trillion shareholder return program. SK hynix immediately issued a clarifying disclosure stating it had "not reviewed any specific details related to shareholder returns."

Yet questions remain about that denial. Given SK hynix's planned shareholder return policy and this year's earnings outlook, a figure of KRW 100 trillion is far from unrealistic.

This is interpreted as a sign that SK hynix is still weighing how much to spend on CAPEX this year. During its first-quarter earnings call, the company said it expects no issue maintaining its principle of keeping CAPEX at around the mid-30% range of revenue this year. Given current market revenue forecasts, that implies CAPEX investment could approach KRW 110 trillion within the year.

Of course, executing the entire KRW 100 trillion on new plant construction within this year alone would be a stretch given the timeline involved. SK hynix has invested KRW 31 trillion over three years through this year in its Yongin Fab 1, which is currently under construction.

There are accounting-based options as well. SK hynix plans to carry out a third-party allotment capital increase of up to KRW 46 trillion next month through a Nasdaq listing of American Depositary Receipts (ADRs). The company has specified that the funds raised will go entirely toward facility investment — including the Yongin Fab 1, the Cheongju P&T7 facility, and EUV equipment acquisition.

An industry source said the key challenge lies in persuading shareholders that shareholder returns are not simply about cash payouts, but about long-term enhancement of corporate value.

Gwak Horyung (horr@fntimes.com)

데일리 금융경제뉴스 Copyright ⓒ 한국금융신문 & FNTIMES.com

저작권법에 의거 상업적 목적의 무단 전재, 복사, 배포 금지

가장 핫한 경제 소식! 한국금융신문의 ‘추천뉴스’를 받아보세요~

{kind=link}