이미지 확대보기

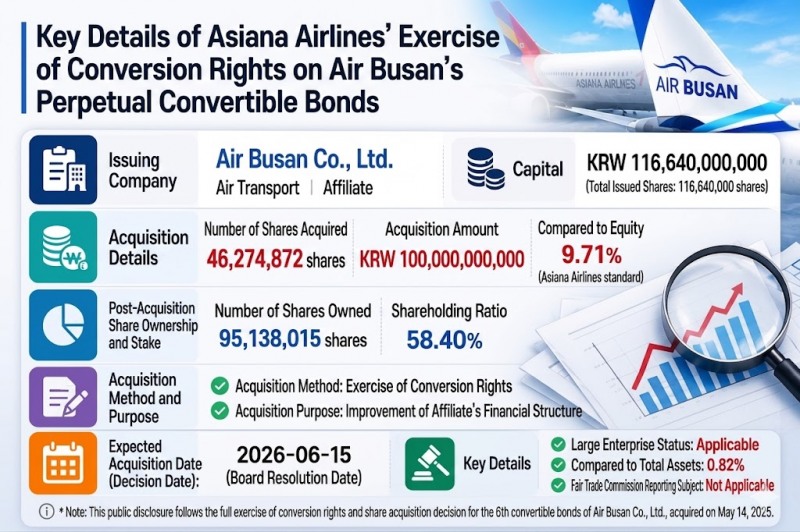

이미지 확대보기According to the Financial Supervisory Service's electronic disclosure system (DART) on the 15th, Asiana Airlines exercised its conversion rights on KRW 100 billion worth of Air Busan perpetual convertible bonds, acquiring 46,274,872 newly issued shares. As a result, its stake in Air Busan rose from 41.92% to 58.40%.

Asiana Airlines stated that the purpose of the share acquisition was to "improve the financial structure of an affiliate," but a closer look at the transaction reveals a structure in which the parent company and ordinary shareholders bear the economic loss.

Shares Converted at a Price 16% Above Market

The price gap at the time of conversion fuels suspicion that the deal is intertwined with the interests of the controlling shareholder.The conversion price was KRW 2,161 per share, yet Air Busan's closing price on the day the conversion was requested stood at KRW 1,863. Asiana Airlines acquired the shares at KRW 298 per share—about 16%—above the closing price. Applying this to the entire KRW 100 billion conversion volume, the valuation loss based on the current market price amounts to roughly KRW 13.8 billion. In other words, Asiana Airlines pushed ahead with exercising the conversion rights despite shouldering a substantial economic burden.

Some interpret this as a preemptive investment in anticipation of rising corporate value, but Air Busan's recent earnings do not support that view. On a separate financial statement basis as of the end of 2025, Air Busan posted a net loss of KRW 22.1 billion, swinging into the red from a net profit of KRW 2.4 billion the previous year.

관련기사

이미지 확대보기

이미지 확대보기Forgoing KRW 5.5 Billion in Annual Interest Income and Step-up Rights

Another point of contention in this decision is that Asiana Airlines' board voluntarily gave up its guaranteed interest income and its right to a "step-up" (a staged increase in the interest rate).The perpetual convertible bonds in question were issued in May last year by Air Busan to raise funds for redeeming existing privately placed perpetual bonds (KRW 50 billion) and for operating capital (KRW 50 billion), with Asiana Airlines acquiring the entire issue. With a coupon rate of 5.53% per annum, the structure allowed for a stable annual interest income of about KRW 5.5 billion, along with the possibility of realizing additional capital gains through share conversion should Air Busan's share price later exceed the conversion price.

Notably, these perpetual convertible bonds included a step-up clause raising the rate to above 8.53% starting in May 2027. Air Busan could have faced the burden of high interest payments or pressure to repay the principal, but this share conversion has effectively eliminated that burden.

By contrast, Asiana Airlines gave up KRW 5.5 billion in annual guaranteed interest income as well as the opportunity for additional earnings from the future rate increase. In effect, the parent company sacrificed a stable cash flow to ease the financial burden of a subsidiary that posted a net loss of KRW 22.1 billion last year. Indeed, Asiana Airlines explicitly stated that the purpose of acquiring shares in another company was to "improve the financial structure of an affiliate." This lends weight to the interpretation that the transaction is one in which the parent company took on an economic burden to support its subsidiary.

The problem is that Asiana Airlines itself—the entity providing the support—is in no comfortable financial position. On the very day it decided to convert the Air Busan perpetual convertible bonds, the company resolved to increase short-term borrowings totaling KRW 150 billion from NongHyup, Hana, and Shinhan banks to raise operating capital. As a result, its borrowings from financial institutions are set to rise from KRW 1.05 trillion to KRW 1.2 trillion.

A company that must immediately raise operating capital through external borrowing displayed a contradictory move: forgoing more than KRW 5.5 billion in annual interest income it could have received from its subsidiary, while instead taking on shares at a price higher than the market value.

Groundwork for the Integrated LCC?… Controversy Over the Ultimate Beneficiary

There is also a considerable view that the benefits of this decision ultimately accrue to Korean Air.The low-cost carriers (LCCs) affiliated with Korean Air and Asiana Airlines are pursuing the launch of an integrated LCC centered on Jin Air in the first quarter of 2027. Should Air Busan be folded into the merged entity while still carrying its step-up risk and loss burden, this would inevitably translate into a financial burden for the future integrated LCC. This raises the question of whether Asiana Airlines' capital was mobilized to remove Air Busan's financial uncertainty in advance.

At the same time, by raising its Air Busan stake to a majority through this share conversion, Asiana Airlines also secured the voting power to quell minority shareholder objections in determining future merger ratios and to lead the integration. Ultimately, if Air Busan—having shed its financial risk on the back of costs borne by Asiana Airlines' ordinary shareholders—joins the merged entity, the benefit will ultimately revert to Korean Air.

In response, Asiana Airlines maintains that the decision took into account the improvement of Air Busan's financial structure and the enhancement of the integrated LCC's long-term corporate value. It also explained that the largest shareholder's exercise of conversion rights at terms above the market price demonstrates its confidence in Air Busan's growth potential and its commitment to responsible management.

Meanwhile, whether the checks-and-balances function of the Korea Development Bank—a major shareholder and creditor of Hanjin KAL, the apex of the governance structure—operated properly throughout this decision-making process has also come under scrutiny. According to the disclosure, the Korea Development Bank holds pledge rights and share-disposal authority over the stake of Chairman Cho Won-tae but stands in an independent position with no obligation to jointly exercise voting rights. Nevertheless, criticism has been raised that it effectively stood by and watched a transaction that could harm the interests of Asiana Airlines' ordinary shareholders.

Lee Yong-woo, head of the Economy Plus Research Institute, pointed out: "Easing the financial burden of a loss-making subsidiary—to the point of borrowing KRW 150 billion that same day just to fund its own operating capital—carries a strong likelihood of a breach of management's fiduciary duty to shareholders and of breach of trust," adding, "It amounts to sacrificing the interests of Asiana Airlines' ordinary shareholders for the sake of a particular controlling shareholder's integration timeline and governance restructuring."

Doo KyoungWoo (kwd1227@fntimes.com)

데일리 금융경제뉴스 Copyright ⓒ 한국금융신문 & FNTIMES.com

저작권법에 의거 상업적 목적의 무단 전재, 복사, 배포 금지

가장 핫한 경제 소식! 한국금융신문의 ‘추천뉴스’를 받아보세요~

{kind=link}

{kind=link}