이미지 확대보기

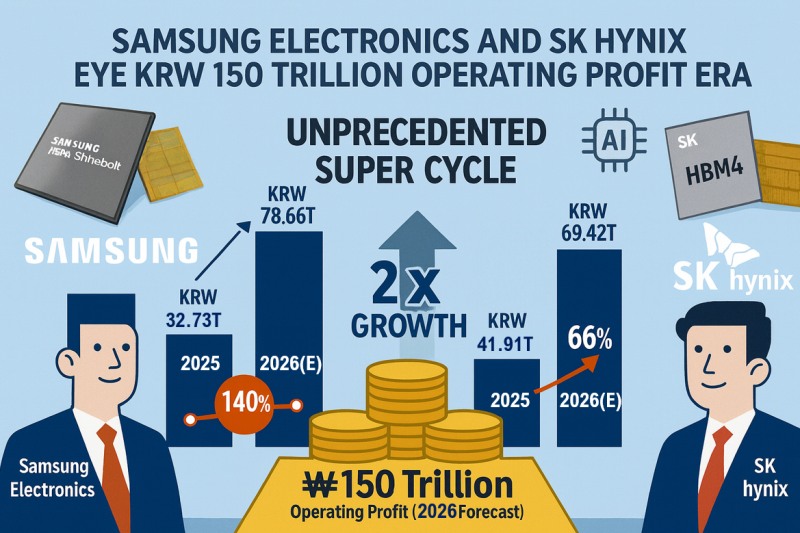

이미지 확대보기According to domestic securities firms' estimates, next year's operating profit for memory manufacturers is projected at KRW 69.42 trillion for SK Hynix and KRW 78.66 trillion for Samsung Electronics, representing increases of 66% and 140%, respectively, compared to this year. These are average values calculated by compiling data from 16 accessible domestic securities firms that updated their corporate analysis reports following both companies' earnings announcements last month.

Korea Investment & Securities, which presented the highest figures, projected combined operating profit of KRW 176 trillion (approximately KRW 81 trillion for SK Hynix and KRW 95 trillion for Samsung Electronics). This represents roughly 90% of the total operating profit (KRW 197 trillion) of all 614 KOSPI-listed companies excluding financial firms in 2024. Securities firms commonly believe that "the memory semiconductor super cycle will continue at least through next year."

The majority view is that SK Hynix will continue to lead the memory semiconductor market in 2026 as well. When considering Samsung Electronics' DS (semiconductor) division alone, some estimates fall below SK Hynix's operating profit projections.

In September, SK Hynix announced it had established the world's first mass production system for next-generation HBM4. Last month, Kim Woo-hyun, SK Hynix's CFO, bolstered optimistic forecasts by stating, "Next year, not only HBM but also DRAM and NAND are virtually sold out."

관련기사

Samsung Electronics Loses D-RAM Top Spot After 33 Years... Will It Struggle All Year?SK Group Doubles Cash Generation on Semiconductor Gains... Energy Sector Increases Borrowing‘Galaxy Z Launch in July’ Roh Tae-moon…Unstable ‘Exynos’ Remains a Concern"Samsung Electronics Bets Big on HBM: Completed Sample Supply of Improved HBM3E, to Be Reflected in Q2 Earnings"SK hynix Posts Over KRW 7 Trillion in Q1 Operating Profit… “Strong Demand for HBM to Persist”

Kyobo Securities also aggressively set SK Hynix's target price at KRW 900,000. However, it maintained Samsung Electronics' target price (KRW 140,000) at similar levels to other securities firms. Choi Bo-young, a research fellow at Kyobo Securities, stated, "SK Hynix will transform into the memory industry's TSMC."

This signifies a shift from traditional memory manufacturing centered on low-price competition through mass production to a foundry-type business structure that supplies high-value-added products that others cannot easily produce through a "pre-order, post-production" method.

Not all forecasts are rosy. HBM profitability is an uncertainty factor. The company is changing its structure from producing "base die" in-house up to HBM3E to outsourcing it to TSMC starting with HBM4.

While SK Hynix stated that "next year's HBM prices are set at levels that can maintain profitability at current levels," cautious views exist. Mirae Asset Securities, which presented the lowest operating profit estimate (KRW 62.6 trillion), predicted that next year's HBM sales will grow only 7% while average selling price (ASP) will decline 7%.

Additionally, iM Securities pointed to declining IT front-end demand due to tariff impacts as a risk, presenting a relatively low operating profit estimate of KRW 62.628 trillion.

Samsung Electronics is also expected to see semiconductors significantly boost overall performance. The surge in general DRAM prices presents an opportunity for greater benefits to Samsung Electronics, which has abundant production capacity. Kiwoom Securities reflected this by projecting Samsung Electronics' next year's operating profit at approximately KRW 80.353 trillion, double this year's figure.

Park Yu-ak, chief research fellow at Kiwoom Securities, assessed, "Samsung Electronics has a considerably high proportion of general DRAM operating profit based on this year's figures, and the magnitude of performance improvement due to the cycle rebound will be greater than competitors."

Samsung Electronics has been showing a trend of recovering technological competitiveness, starting supply of HBM3E to Nvidia from Q3. Additionally, its foundry division has been securing consecutive large orders from external clients including Tesla, Apple, and Nintendo.

However, these positive factors have not been fully reflected in the stock price. While Samsung Electronics' stock price rose 94% this year, SK Hynix surged 260%, with Samsung's increase at about one-third of SK Hynix's. Currently, Nvidia is conducting quality tests on Samsung Electronics' HBM4. While positive signals are emerging both inside and outside the company, the precedent of HBM3E verification taking 18 months remains an uncertainty factor.

The non-memory (System LSI, foundry) division shows improvement trends, but not many forecasts predict a "turnaround to profitability" next year. Among 14 securities firms that estimated non-memory performance, 12 predicted "continued losses."

Samsung Electronics' stock price is expected to show more active movement after proving HBM competitiveness. Noh Geun-chang, head of the research center at Hyundai Motor Securities, stated, "Samsung Electronics' HBM4 will incorporate a base die that applies the foundry division's 4-nanometer FinFET technology, and synergy effects between memory and foundry will be realized."

Gwak Horyung (horr@fntimes.com)

데일리 금융경제뉴스 Copyright ⓒ 한국금융신문 & FNTIMES.com

저작권법에 의거 상업적 목적의 무단 전재, 복사, 배포 금지

가장 핫한 경제 소식! 한국금융신문의 ‘추천뉴스’를 받아보세요~

{kind=link}