![Hyundai Motor Group headquarters. [Photo by Hyundai Motor Group]](https://cfnimage.commutil.kr/phpwas/restmb_allidxmake.php?pp=002&idx=3&simg=2024082315141705194141825007d175114235199.jpg&nmt=18) 이미지 확대보기

이미지 확대보기Standard & Poor's (S&P) has raised Hyundai and Kia's ratings to A- from BBB+, with a rating outlook of 'stable'. In February, Hyundai and Kia received A3 and A- ratings from Moody's and Fitch, respectively.

As a result, Hyundai Motor Co. and Kia Motors Corp. received A grades from the world's top three credit rating agencies this year.

“Receiving A- ratings from all three global credit rating agencies is an official recognition of Hyundai and Kia's excellent financial strength and global market competitiveness,” said a Hyundai Motor Group official.

S&P had previously lowered Hyundai and Kia's ratings to 'BBB+' from 'A-' and assigned a 'negative' rating outlook in late 2019. It was the first time in five years that the ratings were returned to A-. And this is the first time the company has ever received an A3 rating from Moody's.

At the time, Hyundai-Kia's credit rating was downgraded due to declining global sales and profitability. In the U.S., the company's sedan-centric sales system has been stretched to the limit, and in China, three years after the THAAD conflict, sales have been declining every year, let alone recovering. Add to that the Theta2 engine defect, and the company had to rack up trillions in provisions. The red flag was raised on the competitiveness of the business.

이미지 확대보기

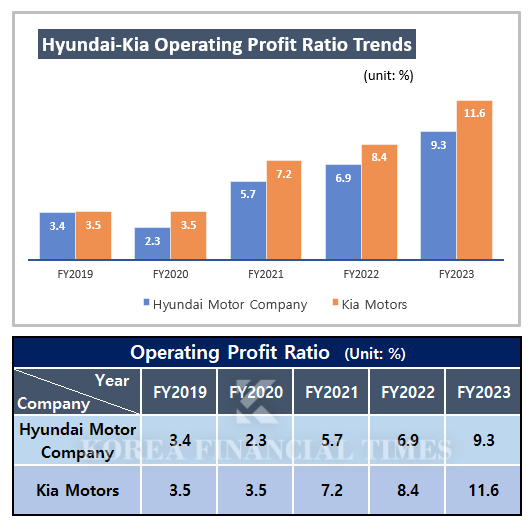

이미지 확대보기Hyundai and Kia's operating margins dropped from 4-6% to 2% in 2018.

It has completely changed in terms of its performance over the past three years. They are among the most profitable in the world, even with limited sales due to the pandemic. Hyundai's operating margin was 5.7% in 2021, 6.9% in 2022, and 9.3% in 2023. Kia posted 7.2% and 8.4% in 2021 and 2022, and a double-digit profit margin (11.6%) last year.

At the center of the turnaround was Hyundai Motor Group Chairman Chung Eui-sun.

Chung was promoted to chairman in 2018 when downward pressure on his credit rating intensified, and took full control of the group's management. He was the first to strengthen his authority and responsibility at each global subsidiary to respond quickly to market trends. Apart from the existing method of mass selling of cost-effective vehicles, he has increased brand awareness by increasing the lineup of mid-sized or higher SUVs or high-end vehicles (Genesis).

The Chinese market, which is a "sick finger," seems to have found the answer. As there has been no effect on new car input over the past few years, it has decided that it will be difficult to recover sales in the Chinese market. Instead, it is expanding exports of vehicles produced at local factories in China to Southeast Asia, the Middle East, and South America.

This is leading to profitability improvement in China's business, which has a severe accumulated deficit. In particular, Kia's Chinese joint venture returned to profitability in the second quarter for the first time in eight years. According to Kia's semi-annual report, Yueda Kia posted a net loss of 17.2 billion won in the first half of this year. Considering that the net loss was 28.8 billion won in the first quarter of this year, it is estimated that it made a net profit of 11.6 billion won in the second quarter.

Gwak Horyung (horr@fntimes.com)

데일리 금융경제뉴스 Copyright ⓒ 한국금융신문 & FNTIMES.com

저작권법에 의거 상업적 목적의 무단 전재, 복사, 배포 금지

가장 핫한 경제 소식! 한국금융신문의 ‘추천뉴스’를 받아보세요~

![‘현대차보다 실적 좋은데 주가는 왜?ʼ 기아는 서럽다 [정답은 TSR]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=284&h=214&m=5&simg=20260724222442045670dd55077bc212411124362.jpg&nmt=18)

![효성, 화학 구했지만 티엔씨 주가 ‘반토막’ [정답은 TSR]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=284&h=214&m=5&simg=20260720100454006620c1c16452b012411124362.jpg&nmt=18)

{kind=link}

{kind=link}