이미지 확대보기

이미지 확대보기Both are leading domestic materials companies whose mainstay is battery cathode materials. They share much in common, from their core business down to their choice of ESS (Energy Storage Systems) as a future breakthrough. So why the current gap in their share-price gains?

The difference is read as stemming from the market's differing views not only of the two firms' materials technology but also of their business competitiveness, including supply chains and customers. While L&F still posts the higher gain for now, market assessment of Ecopro BM is also positive, as it moves into full-scale operation of its European production network and expanded output of LFP cathode material for ESS.

이미지 확대보기

이미지 확대보기'A Firmer Foundation': L&F Shares Up 177% in a Year

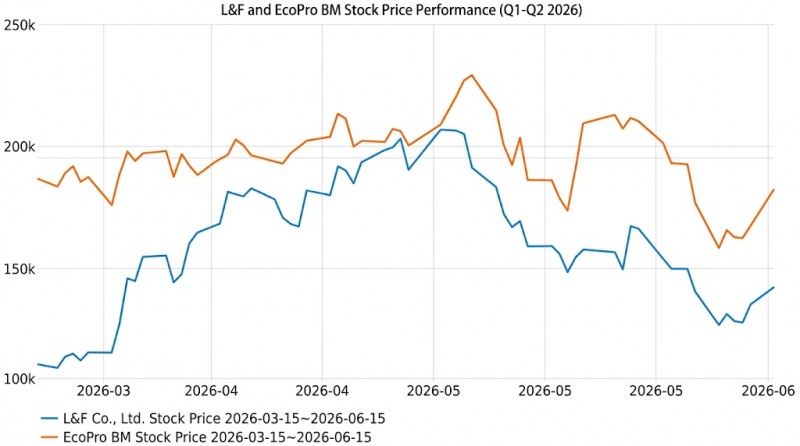

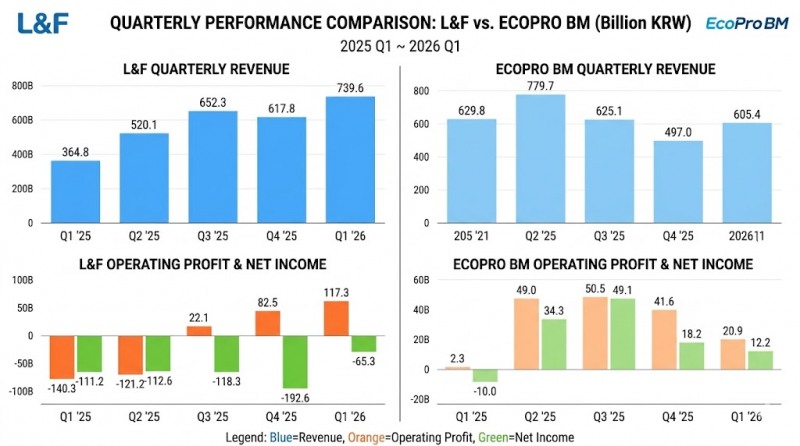

On the 15th, Korea Financial Times tallied the past year's share-price gains for L&F and Ecopro BM using the corporate data platform DeepSearch. Secondary-battery stocks, to which both belong, are being re-rated this year on expectations that the EV chasm is ending and on ESS-driven momentum out of the U.S.Ecopro BM shares rose about 82.8%, from an opening price of KRW 102,000 on June 15, 2025, to KRW 186,500 (the closing price on the 15th) a year later. While Ecopro BM's gain is also a record-setting figure, fellow cathode maker L&F's shares climbed about 177.3% over the same period, from KRW 51,100 to KRW 141,700 — roughly double Ecopro BM's gain.

Set the tally period to about three months, and the gap becomes even starker. L&F shares rose about 34.9% over the past three months, while Ecopro BM actually fell about 0.48%, closer to flat.

관련기사

SK's Holding Subsidiaries Diverge: SK Discovery Falls Behind the PackOnce Samsung's Cash Cow, Galaxy Now Teeters on the Brink of a LossRebounding from a Plunge: Does POSCO Future M's Z-Score Signal a Revival?Lotte Chemical's Losses Mount for 4th Year as Basic Chemical Unit Struggles, Plans Growth Push in Advanced Materials

This divergence is read as reflecting L&F's relatively firmer business foundation amid renewed expectations of a rebound in secondary-battery stocks. The analysis holds that L&F's existing strength in high-nickel ternary (NCM) competitiveness, combined with LFP for ESS, has applied expectations for both the present and the future.

Since the era when NCM batteries were dominant, L&F has leveraged its technology to secure dependable customers in Tesla and LG Energy Solution. It currently exclusively supplies 95%-nickel cathode material for Tesla's flagship ternary models, including the mass-market "Model Juniper." It also supplies most of the cathode material for LG Energy Solution batteries.

Building on its existing strength in NCM cathode material, L&F is reinforcing its technological lead as it nears commercialization of ultra-high-nickel NCM material. Ultra-high-nickel NCM batteries are a premium product category with higher energy density and output than not only conventional NCM but also LFP batteries. Demand for these batteries is rising in future fields such as humanoids, beyond just EVs.

Building on its ultra-high-nickel lead, L&F plans to capture future battery-material markets including humanoids, space, and aviation.

L&F CEO Hur Je-hong said the company "holds world-class technology in terms of cathode energy density," adding that "in future battery markets with high energy density, such as robotics, the company's strengths, including high-nickel, will stand out."

It is also strengthening competitiveness in LFP material, for which demand is rising via ESS, on top of NCM. Notably, L&F is the only domestic producer of LFP cathode material amid the de-China shift in ESS materials. After launching new LFP cathode investment last August, the company aims to build production facilities with annual capacity of 60,000 tons by the third quarter of this year, in two phases. It already completed phase-one facilities capable of producing 30,000 tons of LFP cathode material this past April.

In March, L&F signed a KRW 1.6 trillion cathode-material supply contract with Samsung SDI. It is the first ESS LFP cathode-material supply contract with a non-Chinese cathode maker. The two firms are pursuing a confirmed volume over three years from 2027 to 2029, plus a three-year supply option. Notably, the contract is significant in showing the potential to escape the customer-dependence that had been cited as L&F's weakness.

Starting with this contract, L&F plans to secure a range of customers — not only in ESS but also in EVs and AI data centers — to seize the position of a de-China LFP producer.

이미지 확대보기

이미지 확대보기'European Hub Fully Online': Ecopro BM Targets Both EV and ESS

Ecopro BM, too, intends to steadily expand its business competitiveness and sustain its share-price rebound. Like L&F, its strategy is to secure profitability by expanding supply of high-nickel NCA, centered on Europe, as well as LFP cathode material.First, Ecopro BM is moving to secure European EV customers, centered on its Debrecen plant in Hungary, which recently began shipping high-nickel cathode material.

The Debrecen plant spans about 440,000 square meters and houses Ecopro BM, which produces cathode material; Ecopro Innovation, in charge of lithium processing; and Ecopro AP, which produces industrial oxygen and nitrogen. Of these, Ecopro BM's annual cathode-material capacity totals 54,000 tons across three lines, enough to supply roughly 600,000 EVs.

Daol Investment & Securities analyst Yoo Ji-woong said in a recent report that "with the Hungary plant in operation, Ecopro BM holds the largest available production capacity among secondary-battery materials makers," diagnosing that "a turnaround is now beginning, and it is expected to be the biggest beneficiary of a rebound in the EV market."

The Debrecen plant is, in particular, a strategic base capable of responding to Europe's EV-materials regulations. Amid recently rising EV demand, Europe is mandating the use of EU-made cathode material through measures such as the EU–U.K. Trade and Cooperation Agreement (TCA) and the Critical Raw Materials Act (CRMA).

At the shipment ceremony, Ecopro BM CEO Choi Moon-ho stressed that "even amid fierce global market competition, our top-tier quality and technology have been recognized, and supply is expanding centered on European premium OEM volumes," adding that "we are in talks with major customers for further cooperation targeting the European market and are producing tangible order results."

Alongside this, to strengthen its push into the ESS market, Ecopro BM is focusing on diversifying its lineup — from high-performance product categories centered on high-nickel products to LFP product categories that lead with price competitiveness.

A securities-industry official explained that "both L&F and Ecopro BM are riding an upward trend on the recent tailwinds of a Europe-led EV recovery and rising ESS demand, but at present L&F's corporate value is assessed relatively higher, as it has moved its business foundation and future strategy, including robotics, into full swing." The official added that "Ecopro BM, too, is beginning full-scale response to the EV chasm, starting with the Hungary plant's operation, and its ESS profitability is also coming into view, so expectations for momentum are high."

Kim JaeHun (rlqm93@fntimes.com)

데일리 금융경제뉴스 Copyright ⓒ 한국금융신문 & FNTIMES.com

저작권법에 의거 상업적 목적의 무단 전재, 복사, 배포 금지

가장 핫한 경제 소식! 한국금융신문의 ‘추천뉴스’를 받아보세요~

{kind=link}

{kind=link}

{kind=link}