이미지 확대보기

이미지 확대보기This unusual divergence in Netmarble's valuation metrics is a phenomenon typically seen in companies whose share prices fail to keep pace with asset value during an earnings recovery phase. Industry observers, however, argue that precisely this kind of valuation divergence signals that Netmarble has entered a full-fledged re-rating phase.

The Paradox of an All-Time Low PBR of 0.7 — Rising Asset Value

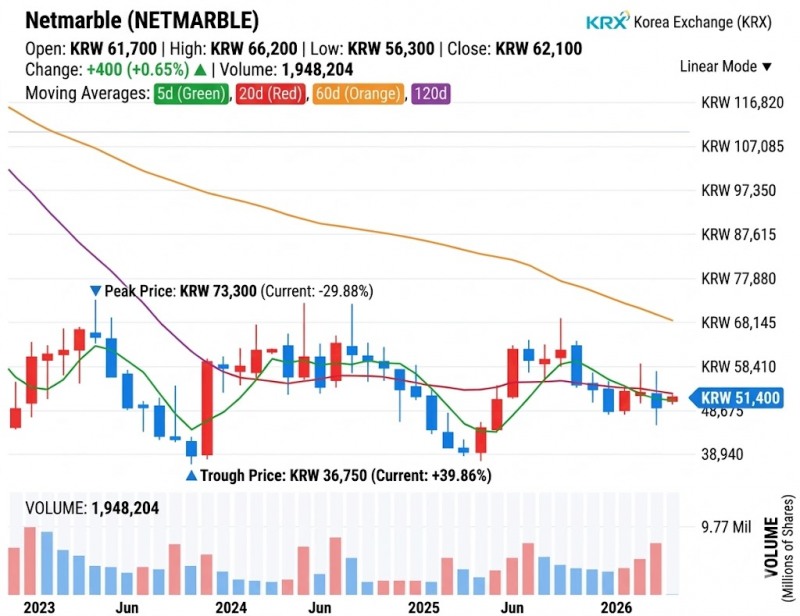

According to the Korea Exchange as of April 1, Netmarble's PBR stands at 0.7x, the lowest level since the company's listing.Netmarble's share price has been stuck in the KRW 50,000 trading range for the past three years following the end of the COVID-19 pandemic tailwind. Meanwhile, the company's book assets have been on an upward trend, reflecting increased stability in holdings such as equity investments and reduced borrowing burdens.

Of particular note are the appreciation in value of Coway, which Netmarble acquired with a long-term vision, and HYBE shares secured through strategic investment. According to Netmarble's 2025 annual report, the fair value of Netmarble's equity-method investments as of the end of last year stood at KRW 1.6086 trillion for Coway and KRW 1.2972 trillion for HYBE, totaling KRW 2.9058 trillion for the two companies combined. This represents an increase of approximately KRW 900 billion compared to KRW 1.9986 trillion at end-2024. Fair value reflects assets appraised at current market prices.

관련기사

Netmarble Tightens Its Belt Even After Returning to ProfitNetmarble's Surprise Leadership Change... Signal for Netmarble Neo's IPO Relaunch?Naver Strikes Disney Deal as Kakao Entertainment StallsSK Hynix Weighs Growth Over Governance in Treasury Share Strategy [Treasury Share Report]'Chung Eui-sun Declares Robot Management Era'... Hyundai Motor Group to Lead Robotics Age with 'Physical AI' [KFT Topic]

Furthermore, through ongoing operational efficiency improvements, the company has reduced its short-term borrowings from approximately KRW 2 trillion to around KRW 1 trillion, thereby improving the quality of its asset base.

"A low PBR also means that the company's fundamental strength is stable, given that asset value exceeds the share price," said an official from one investment banking firm. "In Netmarble's case, while the share price has been range-bound for several years, the fact that the value of its held assets has increased is something that can be viewed positively when assessing future corporate value."

이미지 확대보기

이미지 확대보기PER of 20x 'Overvaluation' Reflects Expectations During Earnings Turnaround

While Netmarble's share price appears undervalued on a PBR basis, it commands a premium over industry peers by the separate valuation metric of PER.PER is calculated by dividing a company's share price by its earnings per share (EPS), indicating how many times the share price is a multiple of per-share earnings. A PER below the industry average suggests the share price is undervalued relative to earnings generated, while a higher PER indicates the share price is overvalued relative to earnings.

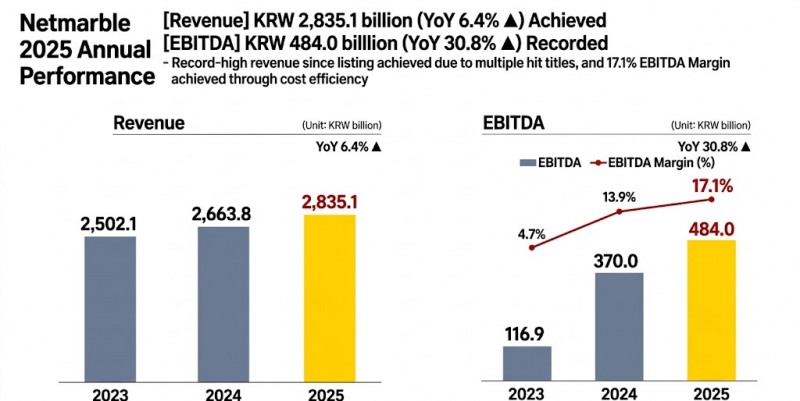

Netmarble's PER stands at approximately 20x, higher than the industry average of around 15x for peers such as NCSoft and Krafton. On the surface, this may appear to indicate an overvalued stock, but it is more accurately described as a "numerical optical illusion" caused by the base effect from the company's worst-ever profitability — which included consecutive annual net losses in 2022 and 2023.

As net profit — the denominator in the PER formula (share price/EPS) — surges, the PER is naturally expected to fall to single digits. This is the process by which a stock that appeared expensive transforms almost instantaneously into "the cheapest stock."

Indeed, Netmarble recorded a net profit of approximately KRW 3.2 billion for fiscal year 2024, when it returned to operating profit, resulting in a PER of around 200x at the time. As net profit surged to KRW 230.8 billion last year, the PER contracted to approximately 20x.

Additionally, PER can appear elevated in turnaround-phase companies as it reflects market expectations for future earnings growth. In Netmarble's case, the turnaround has been underpinned by a new growth driver — expansion built on proprietary IPs such as Seven Knights Re:BIRTH, RF Online Next, and Raven2 — rather than reliance on licensed external IPs. This signals that the market's earnings growth expectations for Netmarble's new growth formula have risen.

"Netmarble is currently pursuing profitability improvement through new titles (PER compression) while holding the safety net of solid assets (low PBR)," the IB industry official said. "The moment these two divergent metrics converge through actual earnings results will mark the true inflection point for Netmarble's share price."

이미지 확대보기

이미지 확대보기'Value-Up' Through Enhanced Shareholder Returns and Platform Diversification

Netmarble is now focused on driving a valuation re-rating through enhanced shareholder returns and platform diversification.First, at its recent annual general meeting, Netmarble announced a significantly strengthened shareholder return policy. The company plans to distribute KRW 71.8 billion in cash dividends for fiscal year 2025, using 30% of consolidated adjusted controlling shareholders' net profit as the funding base for shareholder returns.

In addition, the company plans to cancel all of its approximately 4.7% in treasury shares currently held — within this year — and to expand the shareholder return funding ratio to 40% of consolidated adjusted controlling shareholders' net profit by 2028, implementing cash dividends and share buybacks and cancellations.

Furthermore, Netmarble is focusing on maximizing shareholder value by withdrawing the planned IPO of key subsidiary Netmarble Neo and incorporating it as a wholly-owned subsidiary through a comprehensive share swap.

"We evaluated whether Netmarble Neo could sustain growth after listing and to what extent it could contribute to Netmarble's shareholders," said Kim Byung-gyu, CEO of Netmarble, in a meeting with reporters immediately following the annual general meeting held at Netmarble's Guro-gu, Seoul headquarters on March 26. "We concluded that consolidating through a comprehensive share exchange, rather than a separate listing, would ultimately be most beneficial to Netmarble's shareholders."

The rollout of new titles to diversify revenue streams also continues. In particular, Netmarble is strengthening its global offensive by diversifying platforms beyond its traditional focus on mobile — including eight new titles such as The Seven Deadly Sins: Origin and Mongil: STAR DIVE, which were recently launched for PC and console.

Kim JaeHun (rlqm93@fntimes.com)

데일리 금융경제뉴스 Copyright ⓒ 한국금융신문 & FNTIMES.com

저작권법에 의거 상업적 목적의 무단 전재, 복사, 배포 금지

가장 핫한 경제 소식! 한국금융신문의 ‘추천뉴스’를 받아보세요~

{kind=link}

{kind=link}

{kind=link}