이미지 확대보기

이미지 확대보기However, while Samsung SDI and LG Energy Solution are strengthening product diversification and domestic production—a key evaluation factor—SK On remains relatively quiet. Some in the industry voice concerns that SK On could fall behind not only in this bidding competition but also in the broader ESS transition.

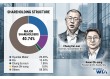

According to the industry on November 19, Korea Power Exchange issued a bidding notice for the second ESS central contract market on November 17 and disclosed the operator selection criteria. The project involves installing approximately 20 GW (gigawatts) of ESS by 2038 across 11 phases, with a total scale of approximately KRW 40 trillion.

Samsung SDI won the bidding war with ternary NCA batteries, unlike competitors who primarily used LFP batteries, which are most commonly used in ESS. NCA batteries have higher energy density and efficiency compared to LFP batteries.

Although structurally more prone to fire risks, Samsung SDI enhanced safety by applying its module-integrated direct spray fire suppression technology "EDI" and thermal propagation prevention technology "No TP." Despite the higher manufacturing cost of NCA batteries, Samsung SDI took the gamble of lowering its delivery price.

관련기사

SK On’s U.S. Battery Plant Hits Full Operation After 3 Years — A Turning Point Toward Profitability?SK On Turns to Private Bonds Amid Market Challenges—Can It Stabilize Its Finances?SK Group Doubles Cash Generation on Semiconductor Gains... Energy Sector Increases BorrowingLG Energy Solution, Samsung SDI and SK-on Aim for 'K-Battery Comeback'

The second round bidding project scale is similar to the first round at approximately KRW 1 trillion. However, there have been changes in evaluation indicators. The proportion of non-price indicators such as safety and domestic ecosystem synergy mentioned above has increased to 50%. For this reason, forecasts suggest that Samsung SDI, which proved its price competitiveness in the first round, will also be advantageous in the upcoming second round bidding.

LG Energy Solution and SK On, which left disappointments in the first round, must restore their pride in the second round. However, while SK On has confirmed domestic ESS production, there are questions about future volume response. This differs somewhat from competitor Samsung SDI expanding its lineup to include LFP while maintaining existing strengths, and LG Energy Solution confirming domestic production and emphasizing mass production capabilities.

이미지 확대보기

이미지 확대보기Particularly, LG Energy Solution, in a similar situation, held an "ESS LFP Battery Domestic Production Promotion Ceremony" at its Ochang Energy Plant together with North Chungcheong Province on November 17, the day of the ESS bidding briefing, introducing plans to strengthen the domestic energy industry ecosystem and technology cooperation. This is a move to secure non-price factor competitiveness in the second ESS bidding war.

LG Energy Solution plans to begin production line construction at the end of this year and commence full-scale operation from 2027. Initial production will start at 1 GWh scale, with plans to gradually expand production scale according to future market demand. The company will also work concurrently on efforts to develop Korea's LFP battery ecosystem for materials, components, and equipment.

What LG Energy Solution particularly emphasizes is mass production capability. LG Energy Solution is the only non-Chinese company with an ESS LFP battery mass production system.

The company began producing ESS LFP batteries at its Nanjing, China plant in 2024, and started product manufacturing at its Michigan, U.S. plant in June this year. LG Energy Solution plans to transplant this "success experience and know-how" directly to its Ochang Energy Plant to develop Korea's ESS industry ecosystem.

SK On is known to be pursuing ESS battery production in Seosan, South Chungcheong Province. However, specific line construction plans have not yet been disclosed.

Additionally, there are criticisms that SK On's ESS transition is lagging behind competitors as poor performance persists. SK On achieved a surprise profit in Q3 this year, but accumulated operating losses for the year reach KRW 490 billion. SK On recently decided to merge with SK Enmove, a profitable affiliate within the group, but maintains a conservative stance regarding ESS transition and related investments.

Jeon Hyun-wook, SK On's Financial Support Division Head, stated regarding ESS transition in an earnings conference call, "ESS transition is currently in the discussion stage. As the ESS market is still in its early stages, we are focusing on minimizing investment scale and maximizing return on invested capital through an efficiency-centered strategy."

He added, "We are also leaving open the possibility of operating production bases in joint venture form and reviewing plans to establish optimal production systems by region."

However, some in the industry point out that SK On's approach could cause it to fall behind not only in the upcoming second round bidding but also in future ESS market competition. Battery and other order-based companies tend to aggressively expand facility investments to enhance production capacity and expand market share. Manufacturers sometimes engage in aggressive bidding, accepting losses to secure market share.

A battery industry official said, "This ESS bidding promoted by the government is a project that judges comprehensive competitiveness, including price competitiveness as well as mass production capability, safety, and contribution to the domestic industrial ecosystem," adding, "Companies that can demonstrate the ability to materialize such comprehensive plans will be advantageous."

Kim JaeHun (rlqm93@fntimes.com)

데일리 금융경제뉴스 Copyright ⓒ 한국금융신문 & FNTIMES.com

저작권법에 의거 상업적 목적의 무단 전재, 복사, 배포 금지

가장 핫한 경제 소식! 한국금융신문의 ‘추천뉴스’를 받아보세요~

{kind=link}

{kind=link}