이미지 확대보기

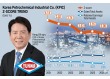

이미지 확대보기Market Cap of KRW 5 Trillion... KRW 59.5 Billion in Operating Losses

Doosan Robotics is a collaborative robot (cobot) company established in July 2015 by Doosan Group as part of its drive to secure new growth engines. After achieving South Korea's first commercial deployment of a collaborative robot in 2017, the company posted revenue of KRW 9.9 billion in 2018, growing to KRW 45 billion by 2022.The market valued this growth trajectory highly. During its KOSPI listing in October 2023, the IPO price was set at KRW 26,000 per share — the very top of the offered price band — raising KRW 421.2 billion for the company. Its current market capitalization stands at approximately KRW 5 trillion, cementing its position as the benchmark collaborative robot stock in South Korea.

Doosan Robotics has gone more than a decade without recording a profit since its listing — a so-called "chronic loss structure" has taken hold. Starting from a peak revenue of approximately KRW 53 billion in 2023, revenue fell to KRW 47 billion in 2024 and KRW 33 billion in 2025, posting three consecutive years of decline and contracting by more than 38% over the past three years.

Meanwhile, losses have continued to widen. Over the same period, operating losses expanded from KRW 19.2 billion in 2023 to KRW 41.2 billion in 2024 and KRW 59.5 billion in 2025. The operating loss margin surged from the 30% range to over 180%.

관련기사

'From Heavy Industry to Humanoids' — Doosan Robotics Charts a New Future in Physical AI [K-Humanoid Wars, Part 3]'Samsung's Bet on the Future' — Rainbow Robotics, Korea's Humanoid Pioneer [K-Humanoid Wars, Part 2]Tesla's Humanoid Rival Has Arrived — Boston Dynamics Eyes $70 Billion Valuation [K-Humanoid Wars, Part 1]

Why the Stock Price Has Held Up...

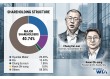

Analysts suggest that the stock's failure to fall as sharply as the deteriorating earnings would imply is not unrelated to this backdrop. Indeed, given an IPO price of KRW 26,000 in 2023, the current share price — hovering around KRW 90,000 despite three consecutive years of losses — represents a return of approximately 240%.The restructuring of Doosan Group's ownership structure in particular has served as a catalyst amplifying share price volatility. A plan to bring Doosan Bobcat, a subsidiary under Doosan Enerbility, under Doosan Robotics as a wholly owned subsidiary has been under discussion since 2024.

Those discussions, however, have been delayed by minority shareholder opposition and regulatory intervention, sending the stock on a rollercoaster ride. A prime example: immediately after the corporate restructuring plan was announced in July 2024, the share price surged 28% in a single session, briefly breaking through the KRW 100,000 level intraday.

In the course of these developments, concerns were raised that Doosan Robotics' valuation had been inflated. Amid criticism that growth potential had been weighted too aggressively in calculating the merger ratio, the restructuring plan was revised multiple times. This illustrates that the market views Doosan Robotics not merely as a standalone listed company but as a strategic asset — a future growth option for Doosan Group.

Industry-wide optimism is also serving as a buffer for the share price. The global collaborative robot market is seen as a blue-ocean opportunity projected to grow at a compound annual rate of 34% through 2030. Insiders broadly expect a turnaround around 2027, underpinned by demand in North American and European markets where labor costs are high.

One industry official noted that Doosan Robotics' current share price should be understood as one that has already priced in both the market's growth potential and expectations for a group-level asset restructuring.

KRW 23.9 Billion Deployed in North American Expansion

Despite the loss controversy, Doosan Robotics is accelerating its overseas investment. The company recently carried out a rights offering of approximately KRW 23.9 billion in its U.S. subsidiary, Doosan Robotics America, to support its North American business expansion.Established in 2022, that subsidiary has been posting widening annual losses — recording KRW 10.7 billion in losses last year. In the second quarter of last year, its total equity turned negative at KRW -2.5 billion, leaving it in a state of complete capital impairment.

According to Doosan Robotics' annual business report, the company's research and development (R&D) investment has also expanded. Last year's R&D expenses accounted for approximately 26% of revenue, a marked increase from 15% the previous year.

Some quarters have raised doubts as to whether the expanded R&D is delivering commensurate results. Critics point out that, compared with Hyundai Motor Group's push — carried out in partnership with Boston Dynamics — to bring physical AI to the commercialization stage, Doosan Robotics' revenue contribution from proprietary technology internalization remains marginal. Investment intensity has risen, but the pace of monetization has been slow, drawing criticism.

To escape this delayed monetization dynamic, Doosan Robotics has played what it calls a card of "fundamental business model transformation." The company has concluded that a one-off revenue model centered solely on hardware sales is insufficient to overcome intensifying global competition and pricing risks, let alone secure stable profitability.

The company is currently transitioning from a hardware-focused entity to a solutions company. After acquiring U.S. automation solutions firm Onexia for KRW 35.6 billion last year and merging its existing North American subsidiary into it, the company has built so-called "turnkey capabilities" spanning robot supply, systems integration (SI), and maintenance. The strategy is to design entire systems in which robots operate — rather than simply selling robots — in order to enhance value creation.

This makes 2026 a particularly pivotal year for Doosan Robotics, as it stands at a decisive crossroads. If orders from North America and Europe expand and the solutions business begins delivering results, the current losses could be reappraised as preemptive investment. Conversely, if revenue stagnation persists, Park In-won's experiment may prove a drag on the group's broader growth strategy.

Jeong Chaeyun (chaeyun@fntimes.com)

데일리 금융경제뉴스 Copyright ⓒ 한국금융신문 & FNTIMES.com

저작권법에 의거 상업적 목적의 무단 전재, 복사, 배포 금지

가장 핫한 경제 소식! 한국금융신문의 ‘추천뉴스’를 받아보세요~

{kind=link}