이미지 확대보기

이미지 확대보기Specifically, during this period, the combined market capitalization of eight listed GS affiliates rose 10%. This is a lackluster performance compared to HD Hyundai (110%) and Hanwha (192%) among the top 10 groups, and even Lotte (22%), which is struggling to find future growth drivers. It also lagged behind Hyosung (290%) and DB (32%), which rank in the 30s in conglomerate rankings, in terms of market capitalization.

GS Group's poor stock performance appears to be due to lowered profit expectations from recessions in core business sectors (refining, retail, construction). The bio sector, which it strategically entered, has also underperformed.

However, even considering this, it is difficult to understand why GS is failing to achieve even one-fifth of the KOSPI's growth rate.

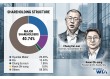

The largest holding in GS Group is GS Corp. (38%). GS Corp. is both a holding company and a company with a significant refining business. It directly controls 100% of unlisted GS Energy, which serves as an intermediate holding company for energy affiliates.

관련기사

GS Corp. has risen approximately 24% this year. According to FnGuide, this falls far short of the average growth rate (73%) of domestic holding companies since the beginning of the year. It is also lower than the growth rate (38%) of S-Oil, which has a similar business structure to GS Caltex.

It's not that GS Corp. lacks positive factors. In particular, if the third commercial law amendment, which is expected to include separate taxation on dividend income, is implemented, it could be considered a beneficiary stock. This is because GS Corp. is a representative high-dividend stock.

GS Corp.'s average dividend yield (based on common stock) over the three years through 2024 reached 6.1%. While there are disclosed dividend standards, they essentially only present minimum dividend amounts, and the company consistently pays a cash dividend of KRW 2,500 per share annually, largely regardless of performance fluctuations.

The background to GS Corp.'s high dividend policy can be linked to its unique governance structure. GS was established when the grandsons of Huh Man-jung, co-founder of (former) LG, separated and became independent from LG. The number of specially related parties holding GS Corp. shares (totaling 53.61% of the equity) reaches 55, including fourth-generation managers who are in the process of sequential management succession.

Because so many people share ownership, it is analyzed to be a structure where it is difficult for any one person's judgment to change the high dividend policy needed to obtain satisfactory dividend income for each individual. If dividend separate taxation is implemented here, the tax burden on the Huh family is expected to decrease significantly.

Nevertheless, investors are paying more attention to owner management's passive shareholder return intentions. This means low expectations for additional shareholder return measures to boost stock prices beyond maintaining the current dividend policy.

In fact, GS Corp. was the last among the top 10 groups to participate in the "value-up" disclosure promoted by Korea Exchange recommendation. The value-up policy content is also not significantly different from before. It contains the statement, "Return at least 40% of average net income (excluding one-time and non-recurring profits) on a separate basis for 2025-2027," and "Minimum dividend is KRW 2,000." The dividend standard is completely identical to the previous 2022-2024 period.

While treasury stock purchases and cancellations to boost stock prices were conducted at some affiliates such as Hugel, GS Corp. has never officially implemented them. With a low treasury stock holding ratio (0.2%), even if the "mandatory cancellation of existing treasury stocks" provision passes in the third commercial law amendment, the effect is not expected to be significant.

Gwak Horyung (horr@fntimes.com)

데일리 금융경제뉴스 Copyright ⓒ 한국금융신문 & FNTIMES.com

저작권법에 의거 상업적 목적의 무단 전재, 복사, 배포 금지

가장 핫한 경제 소식! 한국금융신문의 ‘추천뉴스’를 받아보세요~

{kind=link}

{kind=link}

{kind=link}