Marking its fifth year since establishment, LX Holdings remains trapped in undervaluation. As of end-June, its price-to-book ratio (PBR) stood at 0.38 times. Despite abundant cash and cash equivalents, weak subsidiary earnings are blocking any meaningful re-rating.

While Korean holding companies have rallied on hopes tied to post–Lee administration Commercial Act amendments, LX Holdings has not fully shared in the gains. The stock briefly broke above KRW 10,000 to a year-high in July but has since fallen back into the KRW 7,000 range.

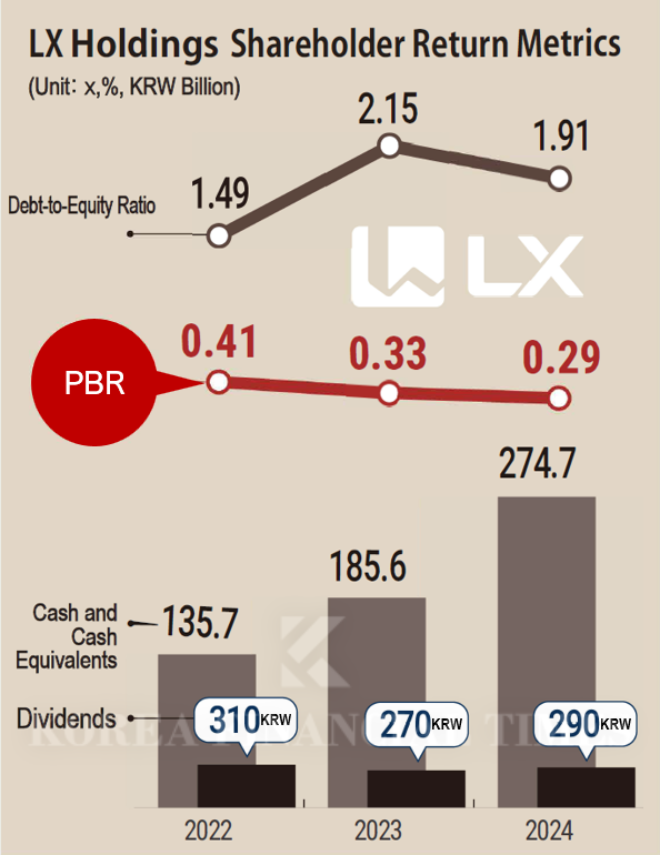

◇ LX Holdings moves to return cash to shareholders

The largest shareholder group of LX Holdings consists of Chairman Koo Bon-jun and 15 related parties (owner family), holding a combined 43.82%. Chairman Koo personally owns 20.37%.His eldest son, President Koo Hyung-mo, holds 11.92%, and his daughter, Koo Yeon-je, holds 8.62%. Retail investors account for 53.86%, more than half. Treasury shares are just 0.06%, and the company has yet to conduct any buybacks or cancellations. Chairman Koo serves as both CEO of LX Holdings and chair of the board.

In February, LX Holdings announced a new dividend policy: over the next three years through 2026, it will return at least 35% of the three-year average net income (on a separate basis, excluding one-offs) to shareholders. In other words, at least 35% of net income will be paid out to shareholders.

On a separate basis, the company posted net income of KRW 41.8 billion last year. Although this was down 40% year-on-year, the dividend per share still increased by KRW 20.

Since its launch in May 2021, LX Holdings has paid year-end dividends annually, distributing KRW 310 per share in 2022, KRW 270 in 2023, and KRW 290 in 2024.

Its balance sheet is solid. As of end-June, cash and cash equivalents stood at KRW 312.1 billion—nearly double the KRW 160.9 billion at inception four years ago. Retained earnings (undistributed) also jumped about 91% over the past year, from KRW 38.0 billion in June last year to KRW 72.7 billion this June.

Financial soundness remains strong. The company stays in a net-cash position, with cash exceeding debt. Its debt-to-equity ratio was 1.49% in 2022, 2.15% in 2023, 1.91% in 2024, and 2.11% in the first half of 2025. Dividend yield is relatively high compared with the KOSPI average of 1.91–2.29%.

Dividend yield is the ratio of annual total dividends to the current share price. LX Holdings posted 3.47% in 2022, 3.78% in 2023, and 4.27% in 2024. The payout ratio—total dividends divided by net income—was 14.20% in 2022, 26.62% in 2023, and 14.07% in 2024.

◇ Subsidiary Performance Is the Weak Spot

As a pure holding company, LX Holdings does not operate standalone businesses; its main income sources are dividends and trademark royalties from affiliates. Given its equity stakes and participation in governance, affiliate performance flows directly into LX Holdings’ results.Key affiliates include the listed LX International (26.8% stake), LX Hausys (33.5%), and LX Semicon (33.1%); and the unlisted LX MMA (50.0%), LX MDI (100.0%), and LX Ventures (100.0%). LX International, in turn, controls LX Pantos (75.9%), LX Glass (100.0%), and Poseung Green Power (70.0%), among others.

In the first half, LX Holdings booked KRW 72.6 billion in dividend income and KRW 15.5 billion in trademark income. Equity-method gains were KRW 117.8 billion, with KRW 741 million in equity-method losses.

For the second quarter on a consolidated basis, revenue was KRW 10.1 billion, operating profit KRW 42.5 billion, and net profit KRW 43.6 billion—down 4.7%, 27.6%, and 27.0% year-on-year, respectively—reflecting weak results at key subsidiaries.

LX International’s operating profit was halved by falling commodity prices and a slowdown in logistics, while LX Hausys swung to a loss amid softer building/interior demand and higher costs.

A weak semiconductor cycle hit LX Semicon hard, slashing operating profit by over 80%, and LX MMA’s profitability deteriorated on petrochemical softness. LX MDI and LX Ventures also remained in the red as new businesses failed to gain traction.

By the numbers, LX International posted revenue of KRW 3.8302 trillion, operating profit of KRW 55.0 billion, and net profit of KRW 56.2 billion, down 6.0%, 57.6%, and 50.3% year-on-year, respectively.

LX Hausys recorded revenue of KRW 819.5 billion and operating profit of KRW 12.8 billion, down 13.0% and 66.1%, respectively, and swung to a net loss of KRW 100 million from a KRW 31.4 billion profit a year earlier.

LX Semicon reported revenue of KRW 378.6 billion, operating profit of KRW 10.2 billion, and net profit of KRW 8.3 billion, down 21.9%, 81.8%, and 81.3%, respectively.

Among unlisted units, LX MMA delivered revenue of KRW 205.7 billion, operating profit of KRW 20.6 billion, and net profit of KRW 18.7 billion. Revenue rose 5.2%, but operating and net profit fell 35.8% and 19.7%, respectively. LX MDI and LX Ventures remained loss-making.

LX MDI posted revenue of KRW 2.2 billion, operating loss of KRW 400 million, and net loss of KRW 300 million. LX Ventures posted revenue of KRW 200 million, operating loss of KRW 300 million, and net loss of KRW 200 million.

The outlook hinges on a cyclical recovery. LX International could improve depending on commodity trends and growth at logistics arm LX Pantos.

LX Hausys also needs a rebound in building-material demand and cost stabilization. LX Semicon would benefit from a global semiconductor upturn, though that appears unlikely in the near term. LX MMA, MDI, and Ventures likewise face a tough path.

An LX Holdings official said, “We will continue striving to enhance shareholder and corporate value.”

Shin Haeju (hjs0509@fntimes.com)

가장 핫한 경제 소식! 한국금융신문의 ‘추천뉴스’를 받아보세요~

데일리 금융경제뉴스 Copyright ⓒ 한국금융신문 & FNTIMES.com

저작권법에 의거 상업적 목적의 무단 전재, 복사, 배포 금지

![용산구 ‘나인원한남’ 88평, 9억 상승한 167억원에 거래 [일일 아파트 신고가]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=284&h=214&m=5&simg=2025071010042800278b372994c952115218260.jpg&nmt=18)

![최호권 영등포구청장, 구청 별관 옥상녹화 조성사업 준공식 참석 [우리 구청장은 ~~]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=284&h=214&m=5&simg=2025082408191103533dd55077bc221924192140.jpg&nmt=18)

![박강수 마포구청장, 녹지 개발 ‘댕댕이 공원' 개장식 참석 [우리 구청장은 ~~]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=284&h=214&m=5&simg=2025082318434900738dd55077bc212411124362.jpg&nmt=18)

![용산구 ‘나인원한남’ 88평, 9억 상승한 167억원에 거래 [일일 아파트 신고가]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=110&h=79&m=5&simg=2025071010042800278b372994c952115218260.jpg&nmt=18)

{kind=link}