이미지 확대보기

이미지 확대보기Samsung SDS (CEO Lee Jun-hee) has secured a war chest of KRW 7.6 trillion, formally launching its transformation centered on artificial intelligence (AI) and mergers and acquisitions (M&A).

The company, which already held approximately KRW 6.4 trillion in cash and cash equivalents, successfully raised an additional KRW 1.2 trillion from global private equity firm KKR. The move is being interpreted not merely as a fundraising exercise, but as a bold strategic bet to fundamentally restructure the company's future business model.

Strong but Slowing Financial Metrics

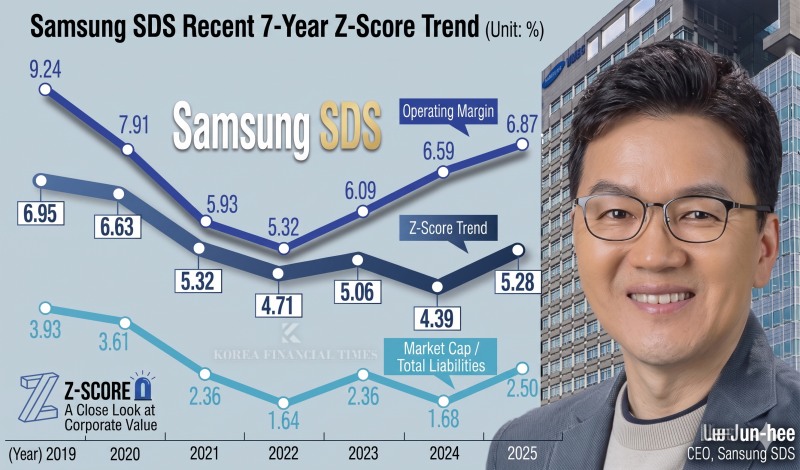

Samsung SDS is, on the surface, a financially sound company with ample cash reserves. However, the market's assessment of the company has shifted. Analysts broadly contend that the company has entered an 'undervaluation phase,' as its reliance on intra-group transactions remains high while profitability and market value have simultaneously stagnated.Warning signals are also evident in the actual data. According to Samsung SDS's Altman Z-Score, as confirmed by Korea Financial Times through AI data platform DeepSearch, the score has trended downward from 6.95 in 2019 to 5.28 last year.

While the company still falls within the financially sound category, downward pressure from its peak is apparent. Samsung SDS's annual Z-Score figures are as follows: 6.63 in 2020, 5.32 in 2021, 4.71 in 2022, 5.06 in 2023, 4.39 in 2024, and 5.28 in 2025.

The ratio of market capitalization to total debt also declined from 3.93 to 2.50. This signals that the market no longer values the company's assets and growth prospects as highly as before — meaning that even without problems in the financial statements, the company's standing in the capital markets has weakened.

These changes are closely tied to the limitations of Samsung SDS's existing business structure. While the company has built a stable track record based on internal IT demand within the Samsung Group, there have been persistent criticisms that its business portfolio is somewhat limited for it to earn a strong growth premium in the external market.

Samsung SDS's intra-group transaction volume last year was approximately KRW 11.3711 trillion, accounting for roughly 82% of total revenue. The proportion, which stood at 86.5% (KRW 11.4910 trillion) in 2023, declined to 80.3% (KRW 11.1047 trillion) in 2024, before edging slightly higher again last year. What has not changed is that intra-group transactions have exceeded 80% for three consecutive years.

KRW 7.6 Trillion Firepower: Why Now?

With financial metrics under downward pressure, the breakthrough Samsung SDS has chosen is a combination with external capital. The company recently decided to issue approximately KRW 1.2 trillion in convertible bonds (CB) to global investment firm KKR.

The core of this deal lies in the strategic intent embedded in the terms that KKR accepted. The conversion price was set at KRW 180,000 per share — a premium of approximately 18% above the market price at the time of the issuance decision. This stands in contrast to typical CB issuances, which are generally priced below market.

Of particular note is the complete absence of a 'refixing' clause — a mechanism that lowers the conversion price when the share price falls. The absence of such an investor protection mechanism suggests that KKR is firmly convinced that Samsung SDS's corporate value will far exceed KRW 180,000 per share within six years.

The inclusion of a six-year ban on transfer and early redemption (put option) further reinforces the analysis that KKR has come on board not merely as a financial investor, but as a long-term value enhancement partner.

Given that Samsung SDS already holds approximately KRW 6.4 trillion in cash and cash equivalents, the essence of this CB issuance appears to lie not in the fundraising itself, but in tapping into KKR's global network and M&A execution capabilities.

KKR has agreed to provide advisory services for Samsung SDS's M&A activities, capital utilization, and identification of global business opportunities over the next six years. Had the structure been designed to pursue short-term profits, such a lengthy advisory arrangement would not have been necessary.

Indeed, KKR has acquired Fujisoft, a major Japanese systems integrator, and has also invested in Ensono, a U.S.-based hybrid IT services company, and DATAGROUP, a German IT solutions provider. This trajectory can be seen as the process of building a portfolio spanning IT services markets across Asia, Europe, and North America.

For Samsung SDS, this network has the potential to directly and indirectly enhance the company's competitiveness in identifying overseas M&A targets, conducting local due diligence, and lowering barriers to market entry.

AI and M&A: A Bold Bet to Reshape the Company's DNA

In particular, the solution Samsung SDS has chosen is AI and M&A. While the existing systems integration (SI) and logistics-centered businesses are stable, their growth ceiling is clear. AI and cloud, on the other hand, can generate high added value and have significant potential to trigger a valuation re-rating in the market.

Samsung SDS has already revealed plans to build AI full-stack capabilities spanning all domains, including AI infrastructure, platforms, and solutions. The pursuit of a national AI computing center in Haenam (South Jeolla Province) and an AI data center in Gumi (North Gyeongsang Province) are part of the same vision. The company plans to invest KRW 5 trillion in infrastructure for the construction of new AI data centers.

Furthermore, the Design-Build-Operate (DBO) business for data centers — announced last year as a new business initiative — has already secured a conceptual design contract for a data center project being developed by a major domestic asset management company, and is currently underway.

When M&A is added to the mix, the pace of change could accelerate further. Based on the KRW 7.6 trillion war chest currently being assembled, Samsung SDS plans to invest KRW 10 trillion in strategic M&A through 2031. The company has also announced its intention to invest KRW 1 trillion to strengthen competitiveness in AX (AI Transformation) services and AI platform and solution businesses, and KRW 4 trillion to secure new growth engines.

Samsung SDS CEO Lee Jun-hee stated, "We will actively leverage KKR's global network and M&A expertise to explore growth opportunities," and added, "To continuously secure future growth engines, we plan to actively pursue the establishment of global business footholds, as well as new businesses such as physical AI and stablecoins, and M&A."

Industry observers view this partnership as a frontal assault on Samsung SDS's long-standing discount factors. Of course, the premise is that the six-year strategic collaboration with KKR will actually translate into concrete overseas M&A results and a diversification of the revenue structure. Should that come to pass, Samsung SDS is expected to shed its image as an IT support affiliate of the Samsung Group and be re-rated as a high-growth AI tech company.

Jeong Chaeyun (chaeyun@fntimes.com)

[관련기사]

가장 핫한 경제 소식! 한국금융신문의 ‘추천뉴스’를 받아보세요~

데일리 금융경제뉴스 Copyright ⓒ 한국금융신문 & FNTIMES.com

저작권법에 의거 상업적 목적의 무단 전재, 복사, 배포 금지

{kind=link}