이미지 확대보기

이미지 확대보기Shifting Cash Flow Engine: POSCO International Surges to 31% of Dividends

According to POSCO Holdings' annual business report released Wednesday, the center of gravity of the group's cash flow is shifting. The contribution from its steelmaking arm, POSCO, which had long been the primary source of group revenue, has declined sharply, while energy subsidiary POSCO International has risen as a new cash cow.Of this, dividends paid by POSCO came to KRW 527.4 billion, representing 55.7% of total dividend income. This compares with dividends of KRW 888.0 billion the year before — when POSCO accounted for more than 63% of total dividend income — indicating a marked reduction in the group's dependence on its steel operations.

The combined effects of cheap Chinese steel imports, a downturn in the domestic construction market, and tightening U.S. tariffs have weighed on POSCO's revenues and dividend capacity.

이미지 확대보기

이미지 확대보기Against this backdrop of steel weakness, POSCO International's turnaround stands out. The subsidiary's dividends last year totaled KRW 298.6 billion, more than doubling from KRW 124.4 billion the prior year, with its share of total dividend income expanding from 8.9% to 31.5%.

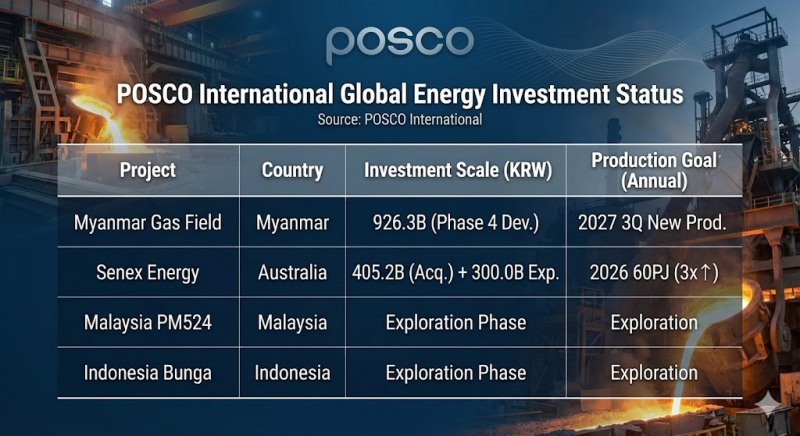

POSCO International posted a record-high consolidated operating profit of KRW 1.1653 trillion last year. The results reflect the full-scale payoff from its strategic pivot away from a trading-centered model toward a three-pillar framework of energy, materials, and food. In particular, strong performance in energy operations — including expanded production from gas fields in Myanmar and Australia — drove the improvement in profitability.

This shift reflects the original intent behind the holding company conversion. When POSCO Holdings was launched in 2022, its stated goals were to reduce dependence on steel and to oversee new businesses such as battery materials and hydrogen. In practice, however, it is the energy segment that has shone first, even as the steel cycle has deteriorated.

Industry observers view this as a successful case of revenue diversification. With energy subsidiary emerging as a functioning "cash engine" despite a sluggish steel market, POSCO Holdings' earnings structure as a holding company is seen as having entered a phase of gradual transition away from its steel-centered axis.

Debt-Fueled Growth: The Mounting Debt Burden

The pursuit of new growth drivers, however, has triggered warning signals across the group's financial indicators. 이미지 확대보기

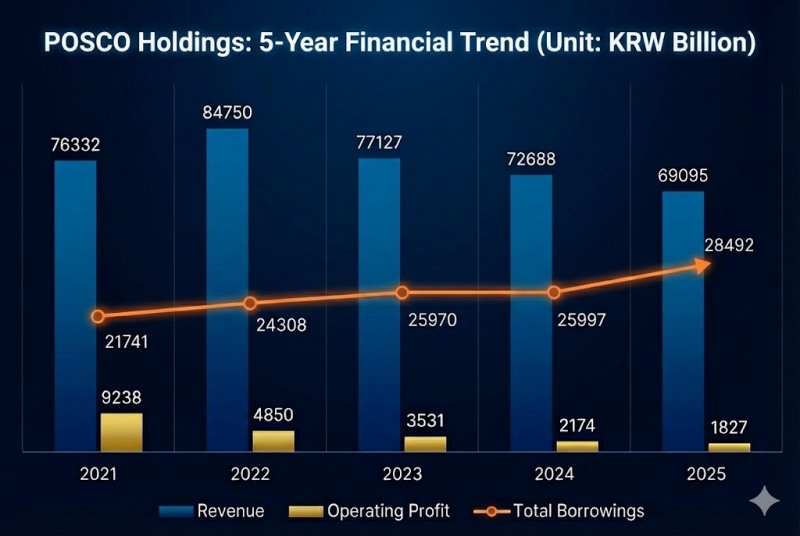

이미지 확대보기Total borrowings at POSCO Holdings over the past five years are as follows: KRW 21.7412 trillion (2021), KRW 24.3057 trillion (2022), KRW 25.9704 trillion (2023), KRW 25.9974 trillion (2024), and KRW 28.4920 trillion (2025).

Total borrowings as of end of last year increased by KRW 2.4946 trillion from the previous year, reaching the highest level since the holding company conversion.

Of this total, short-term borrowings rose 9% to KRW 12.1174 trillion, intensifying short-term liquidity risk given the pressure of maturities falling within one year. Long-term borrowings increased 10% to KRW 16.3746 trillion; while used to fund long-term investment projects, they have prolonged interest repayment burdens in a high-interest-rate environment.

This expansion in borrowings has pushed interest expenses up approximately 26% year-on-year to KRW 1.0914 trillion, from KRW 1.0515 trillion the prior year. The five-year trend in interest expenses is as follows: KRW 439.9 billion (2021), KRW 607.5 billion (2022), KRW 1.0013 trillion (2023), KRW 1.0515 trillion (2024), and KRW 1.0915 trillion (2025).

The more pressing concern is that the rate of decline in operating profit is outpacing the rise in interest expenses. POSCO Holdings' operating profit last year came to KRW 1.8271 trillion, down 15.9% from the prior year. Consequently, the interest coverage ratio (operating profit divided by interest expenses) has fallen to 1.67 times — roughly one-fifth of the 8.6 times recorded in 2022.

A low interest coverage ratio means the company is essentially using earnings from operations to service its interest payments. As financial slack diminishes, capacity for new investment and research and development could contract simultaneously, placing further strain on the group's credit ratings. Ultimately, a growth strategy reliant on debt carries the risk of creating a vicious cycle in which financing costs rise over the long term.

The group's effective cash coverage ratio (ratio of liquid assets to total borrowings) has also continued to decline. Over the past five years, the ratio has moved as follows: 88.60% (2021), 77.20% (2022), 69.60% (2023), 58.73% (2024), and 55.52% (2025). Analysts note that actual liquidity is felt to be even tighter, as the financial assets realistically available for use are further limited due to collateral pledges and other encumbrances.

New Business and Overseas Investment Push Risk Management to the Test

이미지 확대보기

이미지 확대보기POSCO Holdings' direction — transforming from a steel and materials company into a future materials investment holding company — is itself clear.

The issue is pace. The simultaneous pursuit of battery materials and overseas steelworks investments is squeezing near-term cash flows.

Annual capital expenditure (CAPEX) by battery materials affiliate POSCO Future M has consistently exceeded KRW 1 trillion over the past three years, and investment in an electric arc furnace steelworks in Louisiana, U.S. alone amounts to USD 580 million (approximately KRW 860 billion).

On top of this, a joint steelworks project with India's JSW Group has been announced, meaning new funding requirements are continuing to grow.

However, near-term profitability in the battery materials segment remains limited. POSCO Future M's dividends last year amounted to KRW 23.5 billion, an increase over the prior year but still negligible in scale. The dampening effect of slowing electric vehicle demand, which makes a near-term earnings recovery difficult, adds to the burden.

This combination of investment expansion and cash pressure, compounded by group-level debt accumulation, is feeding directly into downside risks to the group's credit ratings.

S&P last year revised its outlook on three POSCO group companies — POSCO Holdings, POSCO, and POSCO International — uniformly to "A- (Negative)," and last month Moody's downgraded its rating to "Baa1 (Negative)." Baa1 represents the lower end of investment-grade territory; two further notches down would place the company in speculative-grade status.

In response, POSCO Holdings stated that it had secured KRW 1.8 trillion in cash through the disposal of low-profitability and non-core businesses in 2024 and 2025, and pledged to raise an additional KRW 1 trillion by 2028.

Ultimately, POSCO Holdings' ability to sustain its growth trajectory will depend on whether it can simultaneously maintain its aggressive investment pace while managing its debt and executing on its monetization strategy. Rebalancing its investment portfolio and securing liquidity through asset disposals have emerged as the pivotal challenges in stabilizing its credit ratings and striking the right balance between financial discipline and long-term growth.

Jeong Chaeyun (chaeyun@fntimes.com)

[관련기사]

- POSCO Holdings Completes 6% Share Cancellation Pledge — But Core Profit Recovery Remains the Missing Piece

- Six Years Locked Away: What Will Hyundai Steel Decide on Its Treasury Shares at This AGM?

- POSCO Pushes Global Expansion to Navigate Safety, Tariff Challenges

- HMM Faces Double-Dip Risk as Performance Mirrors 2023 Downturn

가장 핫한 경제 소식! 한국금융신문의 ‘추천뉴스’를 받아보세요~

데일리 금융경제뉴스 Copyright ⓒ 한국금융신문 & FNTIMES.com

저작권법에 의거 상업적 목적의 무단 전재, 복사, 배포 금지

![SK Hynix Weighs Growth Over Governance in Treasury Share Strategy [Treasury Share Report]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=284&h=214&m=5&simg=20260401095508085350141825007d12411124362.jpg&nmt=18)

![Celltrion's Share Cancellation Undercut by New Issuance Plan [Treasury Share Report]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=284&h=214&m=5&simg=20260325084703088230141825007d12411124362.jpg&nmt=18)

![Kumho Petrochemical's Treasury Shares Face Governance Test After 20 Years [Treasury Share Report]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=284&h=214&m=5&simg=20260324110116057690141825007d12411124362.jpg&nmt=18)

![NearthLab: The Drone Startup That Inspected Wind Turbines — Now Targeting the Global Battlefield [Rising Stars of K-Defense]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=110&h=79&m=5&simg=20260317101811007730141825007d12411124362.jpg&nmt=18)

{kind=link}

{kind=link}

{kind=link}

{kind=link}