이미지 확대보기

이미지 확대보기KT's scale is growing. Revenue has grown steadily over the past five years. Revenue last year increased approximately 8.6% compared to 2020. This is due to simultaneous growth in core telecommunications business (5G, Giga Internet) as well as new businesses such as media, AI/cloud, and B2B specialized services.

KT has been accelerating expansion of AI-based services since launching the AI device 'GiGA Genie' in 2017. After 2022, as AI cloud-based platforms and AI/digital transformation (DX) infrastructure were fully commercialized, the company entered the AI/cloud business expansion stage.

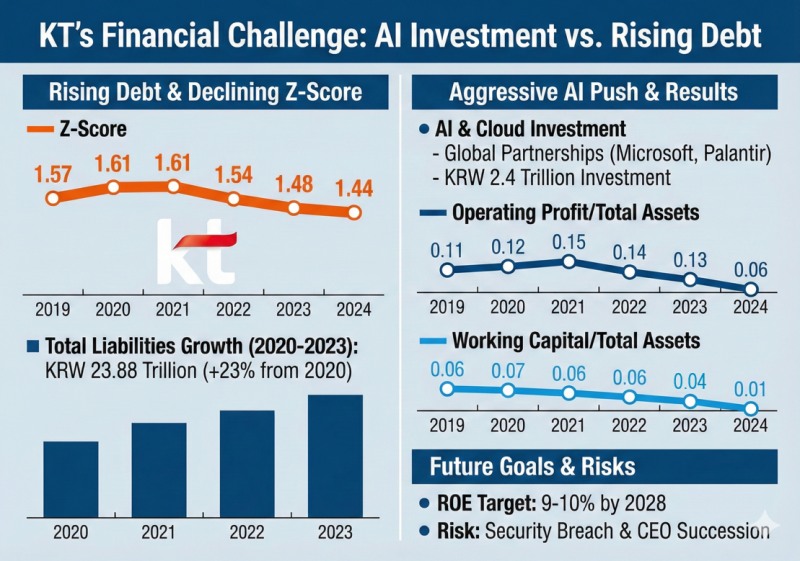

KT has maintained a strategic partnership with MS since last year and agreed to jointly invest a total of KRW 2.4 trillion in AI, cloud, and IT sectors over the next five years.

In March this year, it also began cooperation with Palantir, aggressively entering the AI transformation (AX) market.

관련기사

Low valuation lures investors as KT grapples with hackWhich Korean Companies Are Partnering with Palantir, co‑founded by PayPal alumni?After Missing Out on State-Backed AI Project and Being Left Out of US Delegation, What’s Next for KT CEO Kim Young-shub?Why Did Kakao and KT Fall Short Against Naver and SKT in Korea’s ‘National AI’ Selection?

There are also criticisms that the collaboration results with MS did not meet expectations from the start. The two companies announced development of a Korean language-specialized AI model (SOTA K), establishment of Korean-style cloud services, and establishment of an AX specialized company, but the disclosed results did not resonate much in the market.

Particularly, the plan to establish a separate AX specialized corporation was not realized, and instead, 'KT Innovation Hub' opened in a scaled-down form last month in the West Building of KT's Gwanghwamun headquarters.

Despite large-scale investment, as global cooperation effects have not appeared distinctly, KT's financial burden is growing. Last year, KT's total liabilities were KRW 23.8834 trillion, an increase of approximately 23% compared to 2020.

KT's Altman Z-score, a representative potential insolvency measurement indicator analyzed by Korea Financial News, continuously declined to ▲1.61 in 2020 ▲1.61 in 2021 ▲1.54 in 2022 ▲1.48 in 2023 ▲1.44 in 2024.

While data center infrastructure investment and AI/cloud revenue increased, profitability relative to assets and liquidity deteriorated due to relatively slower growth of application service revenue (IT/AI services, etc.).

Looking at detailed items, 'working capital to total assets' fell from 0.07 in 2020 to 0.01 last year, significantly weakening liquidity indicators. 'Operating profit/total assets' also halved from 0.12 in 2020 to 0.06 last year, confirming the profitability deterioration trend.

From 2021-2023, KT promoted transition to an AICT (Artificial Intelligence + Information and Communications Technology) business structure, and costs increased due to large-scale investment, which led to increases in current liabilities and total liabilities. In 2023, revenue and retained earnings increased approximately 2.8% and 1.7% respectively year-over-year, but could not keep pace with debt growth. Total liabilities increased approximately 7% during the same period.

One-time costs from large-scale voluntary retirement in Q4 last year were reflected, resulting in consolidated operating profit of KRW 809.5 billion, about half the previous year's level. Retained earnings also decreased approximately 12% year-over-year to KRW 13.7798 trillion.

However, KT is maintaining growth trends in total assets and market capitalization following core business expansion.

Total assets steadily increased as investment and asset acquisition in major business groups such as AI/cloud, data centers, and real estate continued, and diversified portfolios in finance, real estate, DX, and content contributed to asset growth.

Market capitalization expanded due to combined effects including expectations for KT's AICT enterprise transformation, record-high revenue last year (KRW 26.4312 trillion), AI/IT new business growth prospects, and strategic partnership with MS.

Strengthened shareholder returns through treasury stock purchases and cancellation are also evaluated to have influenced corporate value enhancement. KT set a target of achieving Return on Equity (ROE) of 9-10% by 2028.

To this end, KT said it would pursue cumulative KRW 1 trillion in treasury stock purchases and cancellation, achieving 9% operating profit margin, expanding AI proportion in IT revenue to 19%, and liquidating non-core assets. A KT official emphasized, "We will secure future competitiveness by making AI/cloud our growth engine, expanding AI data centers, and strengthening infrastructure supply."

The problem is the recent unauthorized micropayment hacking incident. Costs including waiver of penalties for user number portability due to this will be reflected in Q4 this year. 'External pressure trauma' that may occur during the new CEO appointment process is also weighing on KT.

An industry official said, "KT's new CEO must focus on improving financial soundness through market trust recovery and strengthening mid- to long-term new businesses such as AI/cloud immediately after taking office," adding, "Not only expenditures for actual monetary damage compensation but also potential costs necessary for user trust recovery must be considered as tasks."

Jeong Chaeyun (chaeyun@fntimes.com)

데일리 금융경제뉴스 Copyright ⓒ 한국금융신문 & FNTIMES.com

저작권법에 의거 상업적 목적의 무단 전재, 복사, 배포 금지

가장 핫한 경제 소식! 한국금융신문의 ‘추천뉴스’를 받아보세요~

{kind=link}