이미지 확대보기

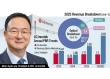

이미지 확대보기According to investment banking (IB) industry sources on the 7th, Hanwha Solutions recently announced a surprise rights offering worth KRW 2.4 trillion. The proceeds are earmarked for capital expenditure (KRW 907.7 billion) and debt repayment (KRW 1.489 9 trillion).

Hanwha Solutions currently holds a credit rating of 'AA-' with a 'negative' outlook. A downgrade would push the company into sub-investment-grade territory (A-tier or below). The average benchmark yield spread between AA- and A+ rated bonds stands at approximately 0.3 percentage points on short-term maturities, meaning a rating cut would directly increase borrowing costs.

More critically, a credit downgrade would deal a severe blow to the company's solar business. The EPC (engineering, procurement, and construction) and power plant development business that Hanwha Solutions has been focusing on is highly sensitive to credit ratings. On various projects, a company's credit rating itself — beyond its role as a financing indicator — can be a disadvantage in the bidding process.

By contrast, Hanwha Solutions' chemicals business is largely unaffected by credit ratings. The rights offering, therefore, is a consequence of weakness in the solar segment rather than the chemicals division.

Hanwha Solutions Weakens Kim Dong-kwan's Standing

While the Hanwha Group has been riding high in the defense and shipbuilding sectors, Hanwha Solutions has continued to underperform. As both are widely seen as ventures driven by Hanwha Group Vice Chairman Kim Dong-kwan, the solar subsidiary's struggles represent a direct blow to his credibility as a manager.Hanwha Solutions is particularly significant because it was the launchpad from which Kim Dong-kwan began to build his reputation as the group's next-generation leader.

FCF — calculated by deducting capital expenditure from operating profit — is the metric that most directly reflects value accruing to investors. While FCF can turn negative during periods of heavy investment, the chronic nature of Hanwha Solutions' deficits is a core concern.

Breaking down the figures: return on invested capital (ROIC) has been declining while weighted average cost of capital (WACC) has been rising. Specifically, net operating profit after tax (NOPAT), the numerator in the ROIC formula, has steadily fallen, while invested capital (IC), the denominator, has grown.

This points to an inefficient allocation of assets — arguably one of the most critical dimensions of corporate management. Compounding the problem, rising interest costs have pushed WACC higher, moving the company further from meaningful value creation.

More troubling still is the prolonged nature of this deterioration. Hanwha Solutions has effectively sustained itself by pouring in capital without meaningfully adapting to changing internal and external conditions.

This dynamic is precisely why the rights offering has failed to win shareholder support. From investors' perspective, years of value erosion leave little basis for confidence in a future turnaround.

It would be unfair to place the full blame for Hanwha Solutions' underperformance on Vice Chairman Kim Dong-kwan, as external headwinds have also been a significant factor. That said, anticipating and responding to such challenges is precisely what is expected of a chief executive — and on this measure, the record falls considerably short.

The Controversy Revives Scrutiny of Hanwha Energy

As the Hanwha Solutions rights offering controversy gains traction, Hanwha Energy has come under renewed scrutiny as well.Hanwha Aerospace announced a KRW 3.6 trillion rights offering in March last year. The controversy stemmed from the fact that Hanwha Aerospace had previously acquired Hanwha Ocean shares held by Hanwha Energy and Hanwha Impact. Critics argued that the transaction ultimately served to consolidate the founding family's control over the group.

Hanwha Energy is 100% owned by the three third-generation heirs — Kim Dong-kwan, Kim Dong-won, and Kim Dong-sun — and in turn controls Hanwha Impact. The Hanwha Aerospace transaction was therefore seen as a mechanism to strengthen the family's dominance.

While both Hanwha Energy and Hanwha Solutions are linked to the solar industry, their roles differ. Hanwha Solutions focuses on manufacturing solar products including ingots, wafers, cells, and modules, as well as providing energy solutions. Hanwha Energy, on the other hand, concentrates on downstream activities such as solar power plant development, construction, operation, and project divestment.

In simple terms, Hanwha Solutions is a key large-scale customer of Hanwha Energy. If Hanwha Solutions' plants were to halt operations, Hanwha Energy would be unable to sell power, directly impacting its revenues. Hanwha Energy holds a 22.16% stake in Hanwha Corporation, which in turn holds a 36.15% stake in Hanwha Solutions.

From shareholders' perspective, the rights offering dilutes per-share value. But for the third-generation heirs managing the group, it is a matter of necessity.

A fixed-income portfolio manager at an asset management firm commented that a rights offering is "the highest quality form of capital replenishment, superior even to earnings improvement." He added that given the deteriorating cash flow environment, "the equity issuance is a financing strategy that is entirely favorable to creditors." He also acknowledged that "it is entirely understandable that shareholders, having received no meaningful returns over an extended period, would find it difficult to support this rights offering."

Lee Sungkyu (lsk0603@fntimes.com)

[관련기사]

가장 핫한 경제 소식! 한국금융신문의 ‘추천뉴스’를 받아보세요~

데일리 금융경제뉴스 Copyright ⓒ 한국금융신문 & FNTIMES.com

저작권법에 의거 상업적 목적의 무단 전재, 복사, 배포 금지

![[Petrochemicals: A Shifting Landscape] Korea's Petrochemical Restructuring Accelerates as Middle East Crisis Bites](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=284&h=214&m=5&simg=20260406091454015940141825007d12411124362.jpg&nmt=18)

![SK Hynix Weighs Growth Over Governance in Treasury Share Strategy [Treasury Share Report]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=284&h=214&m=5&simg=20260401095508085350141825007d12411124362.jpg&nmt=18)

![Celltrion's Share Cancellation Undercut by New Issuance Plan [Treasury Share Report]](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=284&h=214&m=5&simg=20260325084703088230141825007d12411124362.jpg&nmt=18)

![[Petrochemicals: A Shifting Landscape] Korea's Petrochemical Restructuring Accelerates as Middle East Crisis Bites](https://cfnimage.commutil.kr/phpwas/restmb_setimgmake.php?pp=006&w=110&h=79&m=5&simg=20260406091454015940141825007d12411124362.jpg&nmt=18)

{kind=link}